Recommended

Blog Post

A New ‘Decision Tree’ Tool to Improve Financial Inclusion

Financial inclusion is a crucial driver of economic development, and many countries are implementing ambitious strategies to increase their populations’ use of financial services, especially digital financial services. But the results are mixed, with impressive gains in some countries while others lag behind. A pressing question for policymakers is how to diagnose the country-specific root causes of the digital financial inclusion gap to adequately prioritize needed actions and reforms.

A Decision Tree for Digital Financial Inclusion Policymaking is a comprehensive analytical framework to diagnose the factors significantly impeding improvements in digital financial inclusion in specific country settings. The methodology has been published as a CGD working paper and applied to five case studies: Ethiopia, India, Indonesia, Mexico and Pakistan.

The decision tree methodology

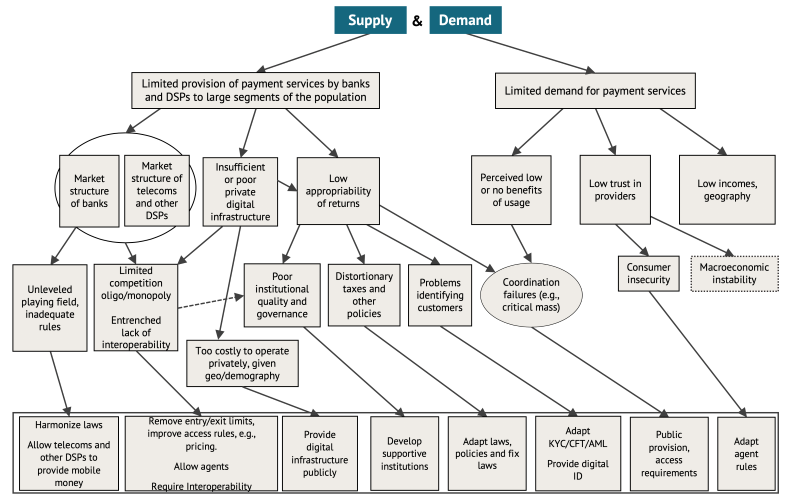

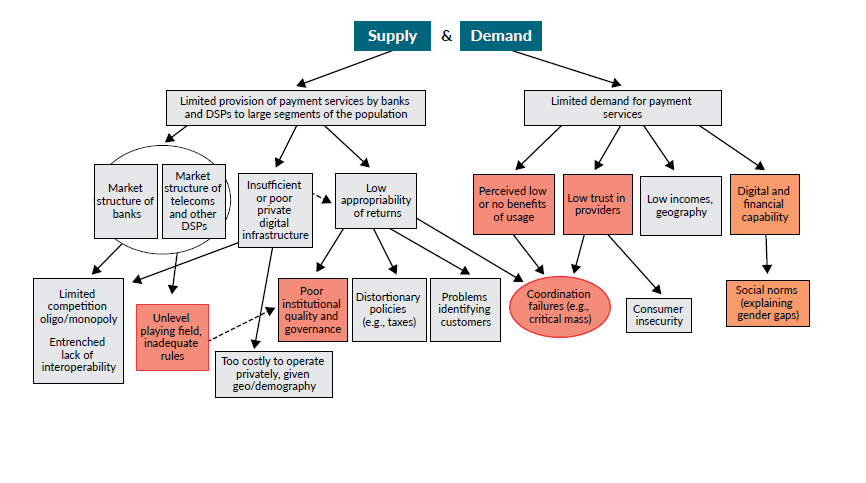

The decision tree is constructed on the assumption that the actual usage of digital financial services (DFS) in a country is determined by both supply and demand factors.[1] Since there is a variety of DFS (e.g., payments, store of value services, credit, insurance) and the factors affecting the use of each vary, each service requires a specific tree. Figure 1 presents an abridged version of the decision tree for digital payment and transfers.

Figure 1. The decision tree for digital payment services, abridged

Applying the methodology: A deductive approach

After identifying a problem of low financial inclusion, initial potential causes (the upper branches of the tree) should be studied. On the supply side, potential constraints include problems in the market structure of key providers (including both banks and non-banks digital service providers), low or poor provision of digital infrastructure, and problems in appropriating returns from the offering of the services. On the demand side, potential constraints include customers’ perception of low or no benefits from using DFS, lack of trust in providers, low levels of income, and residence in challenging geographies.

Each of these constraints can, in turn, be explained by additional factors (the next set of branches).[2] Thus, the tree moves from aggregate outcomes (low inclusion and its general causes) to more specific factors that explain potential constraints. Following this deductive, top-down approach and analyzing each branch of the tree, analysts can reach the binding constraints, the root causes, of low inclusion and enact effective policy solutions.

Identifying binding constraints

The optimal policy response to binding constraints varies depending on whether these constraints are on the supply or demand side. Answering that question requires an examination of prices in the market for DFS.

Low usage is consistent with both demand and supply problems, which can also co-exist. But as a guiding rule, the low usage of a DFS can be attributed to supply-side constraints if the fee charged for using the service is high relative to either a similar service or the usual price charged in other countries at similar levels of development. In this case, providers are only willing to supply the service at a high price, excluding large segments of the population from its use. On the other hand, if the fees are relatively low, this likely indicates a demand problem, where users are unable or unwilling to use the service, despite its low price.

In addition to the fees for using the services, there are indirect costs that affect the market equilibrium and that need to be considered. These include the cost of digital infrastructure (the fixed costs of buying a cellphone plus the variable costs of the monthly rates), the cost of procuring necessary documentation, and travelling expenses. These may make the overall cost of using DFS extremely high, even if the fee is low. In India, indirect fixed and variable costs could add up to 50 percent of the annual income of the ultra-poor, making the usage of DFS prohibitively expensive for this segment of the population.

After the initial analysis of prices, three guiding principles (based on Hausmann et al. (2008)) can help to determine whether a constraint is binding. A constraint is likely binding if:

- Relaxing it results in a significant improvement in the usage of the service, or other relevant behavior. For example, if reducing or eliminating certain taxes on digital payment services causes a sharp rise in the usage of the service. The case of Pakistan, where the imposition and withdrawal of a withholding tax on financial transactions significantly affect the usage of cash versus formal finance, illustrates this principle.

- Market participants are trying to overcome or bypass the constraint. Analysts should assess whether individuals are using alternative services or going through complex processes to avoid the constraint. For example, in Mexico, to bypass a regulatory binding constraint, some digital payment providers have either changed their model of operations or are forming alliances with financial entities that are not subject to the constraint.

- Market participants less affected by the constraint are thriving. When those not affected by a constraint have considerably higher levels of inclusion than those who suffer it, the constraint is likely binding. For example, in Indonesia, while the usage of digital payment services is higher in Java, the low provision of digital infrastructure in remote and rural areas proved to be a binding constraint for populations outside Indonesia’s main island.

Indicators including hard data and perception surveys are needed to perform these tests. These indicators should be employed in benchmarking exercises against comparable countries and, coupled with stakeholder interviews and country-specific literature reviews, are necessary to fully assess each of the branches of the tree, the links between them, and which are binding. [3]

Country case studies

Analysts from five countries in three regions prepared detailed case studies that examined the current state of digital financial inclusion in their countries and the multiple constraints they face, using the decision tree approach. These five countries (Ethiopia, India, Indonesia, Mexico, and Pakistan) all have low levels of digital financial inclusion compared to countries with similar degrees of development. The case studies, which focus on usage metrics for digital payments and store of value services, indicate that over 50 percent of the population in each country is digitally financially excluded (Figure 2). These five countries alone roughly account for one billion adults who do not use digital financial services.

Figure 2. Percentage of adults that are digitally financially excluded using country-specific metrics (numbers in parenthesis indicate millions of adults)

Sources: individual case studies, several national sources and United Nations World Population Prospects (2021).

Notes: Ethiopia measures mobile account ownership using National Bank of Ethiopia’s statistics for 2020; Pakistan reports the general level of financial inclusion in the 2020 Financial Inclusion Insights (FII) survey; Mexico uses the Findex metric of the percentage of individuals who made or received digital payments for 2017; and India and Indonesia indicate the usage of digital payment services based on the 2018 FII surveys.

To illustrate the application of the decision tree methodology and what it can reveal, we summarize here finding from Ethiopia and India. Binding constraints are highlighted in red and severe constraints, which might be binding for specific subpopulations, are in orange. Because the methodology is applied to specific country-settings, in conducting their analyses the authors found additional interrelations between branches of the tree and even new branches not included in the original tree.

Ethiopia

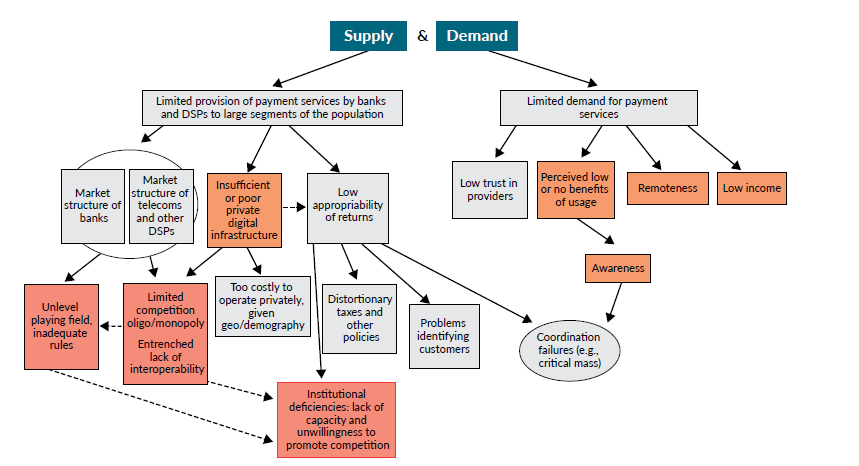

In Ethiopia, institutional problems are the binding constraint (Figure 3). The lack of capacity of key regulators and supervisory authorities and the unwillingness of the central government to promote competition intertwine, limiting competition in the digital infrastructure and financial services sectors, and fostering an unlevel playing field between providers. This lack of competition, in which state-owned enterprises dominate both sectors (Ethio Telecom and the Commercial Bank of Ethiopia respectively), is, in turn, associated with high prices and low provision of digital payment services.

Figure 3. Decision tree as applied to Ethiopia

Inadequate regulatory and supervisory capacity serves to justify the closed nature of the Ethiopian markets and further motivates the reluctance to open these industries to competition from the private sector. This unwillingness is rooted both in economic causes, as these industries provide significant revenues for the government, and in the political interest of controlling key sectors.

While supply-side constraints dominate, some demand-side factors constitute severe constraints affecting certain populations and areas. In rural areas and specific regions like Afar and Somali, few perceived benefits (linked to the low awareness about DFS), the long distance to providers, and low-income levels are severe constraints.

India

In India, there are binding constraints in both the supply and the demand sides (Figure 4). First, an unlevel playing field favors the banking sector and reduces competition and innovation that could support lower-income and marginalized people. The unlevel playing field is potentially rooted in institutional weaknesses and the nexus of control of the government and the banking system, as the public-owned banks are key players in the market.

Figure 4. Decision tree as applied to India

Second, under this deficient market structure, the outreach and inherent business model of digital payments do not provide sufficient perceived benefits to most of the population. A perception of low benefits combines with a lack of trust in providers and prevents the formation of a critical mass of users. As a result, coordination failures (between providers, merchants, and potential users) are binding, especially in urban settings.

In India, a new branch, which was not contemplated in the original tree, was added to explain why women display different behavior towards DFS. It is found that social norms, limiting women’s participation in financial decisions, and even hindering their capability to have and use mobile phones, is a severe constraint for their financial inclusion.

The Ethiopian and Indian studies have both marked similarities and differences with the other three case studies. Pakistan, like Ethiopia, finds the binding constraint to be institutional deficiencies; but, while in Ethiopia these result in a lack of competition, in Pakistan these structural issues are reflected in distortionary policies that promote informality and a preference for cash that harms financial inclusion. Mexico and Indonesia, like India, find unlevel playing field issues to be binding. In both countries, regulatory roadblocks are clearly reflected in limitations to the services that non-bank providers can offer, as they face restrictions on cash-out services and on agent networks expansion.

Pakistan and India share significant demand-side constraints, like social norms that hinder women’s ability to be digitally financially included. Yet, while in India some demand-side constraints are binding, in Pakistan obstacles on the demand side (in particular, a low technical literacy and a low awareness about the products) are only severe constraints for older and less-educated subpopulations.

Lessons learned

The development of the decision tree methodology and its application in the case studies reveal important lessons.

1. Data is key, but scarce and sometimes inadequate

There were substantial data limitations in every country studied. First, Findex is the only database that offers comparable data on the usage of DFS and account ownership for a wide range of countries. Even national authorities often rely on this dataset. While this highlights Findex’s importance, it is far from ideal—Findex’s last available data is from 2017 and there are almost no alternative sources.

Second, the studies made it clear that data on usage is more relevant than ownership information. In several countries studied, there are large numbers of dormant accounts in different services. However, data on usage is also much harder to obtain.

Third, collecting DFS price data is an arduous manual task in which researchers must visit providers’ webpages, which are often not up to date or easily accessible. This makes performing international comparisons particularly difficult.

Finally, there are very few demand-side surveys that can be used in cross-country comparisons. The Financial Inclusion Insights (FII) is the most complete one, but it is only available for a few countries. While most of the case studies exploited this data, the international and regional comparisons that can be made with it are limited.

In sum, to further the understanding of constraints and to effectively improve digital financial inclusion, stakeholders should invest in initiatives that support collection of data on DFS prices and usage. Moreover, initiatives that encourage providers and regulators to facilitate this process, especially through improved transparency, are needed. Comprehensive surveys like Findex and FII are absolutely crucial, but more work is required—particularly to provide a better sense of demand-side constraints and improve access to usage and price data.

2. Engagement with stakeholders is paramount

Stakeholders (providers, users, and regulators of DFS as well as of digital services more broadly) need to be involved in any application of the decision tree methodology. In the preparation of the case studies, stakeholders proved very valuable since they served as a source of priors that helped in the design of the country-specific tree and provided a fresh look to the methodology, pointing to blind spots in the framework and explaining their own relevant priorities. For instance, policymakers’ decisions often involve trade-offs, which ought to be understood to paint an accurate picture of a country’s financial inclusion landscape.

3. The trees allow for additional country-specific branches

Not only does each financial service require the construction of its own tree, but each country might also require a slightly modified tree, as seen in the examples above. The original trees serve as templates that can be adjusted to accommodate the peculiarities of specific financial services and country settings. It is possible that a case study will end up with a tree that is somewhat different from the one it started with—applying the principles, considering indicators, and discussing with stakeholders could shape the tree in different manners.

4. Binding constraints can be found outside the DFS market

The decision tree looks at the entire economy, searching for obstacles that may directly or indirectly impede improvements in digital financial inclusion. It is possible, therefore, to find the binding constraints in areas of the economy that may not be directly related to the DFS market. Since the tree can be adapted and expanded, analysist should approach the methodology with an open mind.

For example, in Pakistan, the binding constraint, institutional weaknesses, is reflected in distortionary policies that have had the unintended consequence of encouraging a preference for cash over the use of formal financial channels among most people. Thus, authorities should acknowledge and evaluate the impact of diverse policies on financial inclusion, even if they are seemingly not related to it. Financial inclusion strategies need to be incorporated into broader policy conversations as an integral part of development policies.

[1] The decision tree methodology builds on Hausmann and coauthors work on growth diagnostics. See Hausmann, Rodrik, and Velasco, 2005. “Growth Diagnostics.” Center for International Development, Harvard University; and Hausmann, Klinger, and Wagner, 2008. “Doing Growth Diagnostics in Practice: A ‘Mindbook.’” Center for International Development, Harvard University.

[2] In this set of branches, the tree includes an obstacle that is particular to digital platforms: coordination failures, which incorporates elements of both the demand and the supply-sides. Coordination failures occur most notably when the market lacks a critical mass of customers who are reluctant to adopt the service because there are not sufficient counterparts (merchants or individuals) to transact with and, simultaneously, this lack of critical mass impedes providers to reach necessary economies of scale making them also reluctant to enter the market.

[3] Some countries recently started using this type of framework. For example, Mexico has incorporated a decision tree approach in its national financial inclusion strategy.

Topics

CITATION

Rojas-Suarez, Liliana, and Alejandro Fiorito. 2021. Building Digital Financial Inclusion: A Decision Tree Approach. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}