Recommended

Blog Post

Climate Finance Is the Elephant in the Room at COP26

The Intergovernmental Panel on Climate Change (IPCC)’s Sixth Assessment Report on climate change made one thing very clear: development will be crucial for coping with climate change.

Poorer countries see more deaths in the wake of natural disaster, are ranked as the most vulnerable to climate change by various climate vulnerability indices, and are more reliant on industry and income-sources that are the most likely to me impacted by climate change, such as agriculture. Development has always been important, but now the stakes are even higher.

This blog briefly reviews various projections for economic development to 2050 and takes a closer look at arguably the most authoritative assessment of what the longer-term future might hold for development, the Shared Socioeconomic Pathways (SSPs), produced for the IPCC. This forms part of our work on the future of development, which attempts to address key questions including: What can we expect from economic growth over the coming decades, and what implications will this have for development and multilateral agencies? What will financing needs be, who will provide it, and are country-level or global challenges (including climate) more pressing?

Growth matters

There is more to life than economic growth, but far from being a technocratic, abstract number, it is still a crucial determinant of many of the things we care about. There are concrete realties behind the numbers: for instance, Hans Rosling called $40 a day the “wash line”, above which washing machines become affordable. Economic growth is of central importance for poverty reduction; useful in alleviating multiple dimensions of deprivation and expanding real human capabilities. It can promote the spread of democracy, open societies, and peace—but it is also tightly associated with greenhouse gas emissions.

The majority of global inequality is still composed of differences in average incomes between countries, rather than inequality within countries—which is why catch-up growth is so crucial. Even seemingly small differences in growth rates have huge implications over the different the timeframes in which poorer countries can reach current high-income levels, and in turn their ability to cope with climate impacts.

The future of economic growth is therefore a key determinant of human welfare, and the emissions intensity of growth will also be an important factor in climate outcomes.

Overview of existing growth projections

So what long-run projections of economic growth currently exist? Projections of GDP are available from a number of key sources, outlined in Table 1 below.

Several multilateral institutions regularly publish GDP growth projections (e.g. the IMF, World Bank, and UN), but these are shorter-term forecasts covering only between two to five years into the future. Further, forecasts with longer time-horizons (e.g. from the OECD and researchers at PwC and Goldman Sachs) often tend to focus on a limited number of large economies, such as those in the OECD and G20.

Table 1. Overview of GDP projections

|

Forecast Source |

Latest Publication |

Indicator* |

Time Horizon |

Country Coverage |

|

Short-term Projections: |

||||

|

WB Global Economic Prospects |

Real GDP growth rate |

2023 |

148 countries |

|

|

UN World Economic Situation and Prospects |

Real GDP growth rate |

2023 |

178 countries |

|

|

Medium-term Projections: |

||||

|

USDA ERS International Macroeconomic Data Set |

GDP per capita (2015 USD) |

2033 |

181 countries |

|

|

IMF World Economic Outlook |

GDP per capita (2017 USD, PPP) |

2026 |

196 countries |

|

|

Long-term Projections: |

||||

|

OECD Economic Outlook |

GDP (2010 USD, PPP) |

2060 |

48 countries |

|

|

Shared Socioeconomic Pathways Database |

GDP per capita (2005 USD, PPP) |

2100 |

184 countries |

|

|

PwC: World in 2050 |

GDP per capita (2016 USD, PPP) |

2050 |

32 countries |

|

|

Kharas (2010) |

GDP per capita (2005 USD, PPP) |

2050 |

145 countries |

|

|

Goldman Sachs: Path to 2050 |

GDP per capita (2003 USD) |

2050 |

10 countries |

*Notes: (a) Some forecasts are only for aggregate GDP (WB GEP, UN WESP, OECD Economic Outlook). To calculate per capita figures these GDP forecasts must be combined with independent population projections; (b) Some forecasts are not calculated using PPP (GEP, WESP, USDA, Goldman Sachs).

Compared to these two groups of forecasts, the US Department of Agriculture (USDA) strikes more of a balance with its decade-long time horizon and coverage of 181 countries. And Homi Kharas has also produced GDP per capita projections to 2050 for 145 countries—though the data for these projections has not been published. Yet perhaps the most useful set of long-term growth projections to date come from the Shared Socioeconomic Pathways (SSP) Database.

The SSPs are a range of plausible future scenarios developed for the Intergovernmental Panel on Climate Change (IPCC) which assume the absence of any climate policy. They comprise five stylized narratives (SSP1-5), which generate a set of conditional forecasts based on certain assumptions holding true (for instance, on the rate of frontier growth and convergence speed). SSP2 represents a business-as-usual scenario, where current trends continue; whereas SSP5 is the most optimistic for global growth, and SSP3 the most pessimistic. Based on these scenarios, three different modelling teams developed century-long GDP projections to 2100 for each of the SSPs, out of which one set of projections was selected as representative. The chosen projections cover 184 countries and are based on the OECD’s ENV-Growth model (i.e. an augmented version of the Solow model, a workhorse model of economic growth that assumes that in the long run, growth is driven by exogenous technological change).

Shared socioeconomic pathways: Five visions of the future

The SSPs stand out in terms of the detail and depth of their projections. So, what do they say about the future of development?

By design, the global economic fortunes vary greatly between SSPs, as they are intended to cover a wide range of plausible growth scenarios, although all but one suggest higher growth in the median country’s income than in the last thirty years . Under the most optimistic scenario (SSP5), growth in median country’s GDP per capita will average around 4.6 percent, whereas the under the least optimistic (SSP3), the median country will grow at around 1.7 percent on average. While the difference does not seem large in any one year, when compounded over three decades, this is the difference between growing by 70 percent, and 290 percent. In the former case, the median country (currently between Maldives and Albania) would, by 2050, be roughly as rich as Argentina is today (with a GDP per capita of $19,000, at 2017 prices PPP). In the latter, it would be as rich as Canada ($46,000).

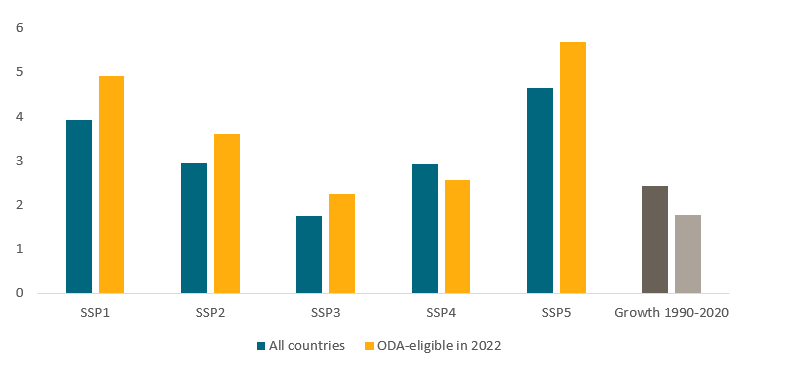

Figure 1. Compound average growth rates 2020-2050 for median country, by SSP

What about future growth in lower-income countries?

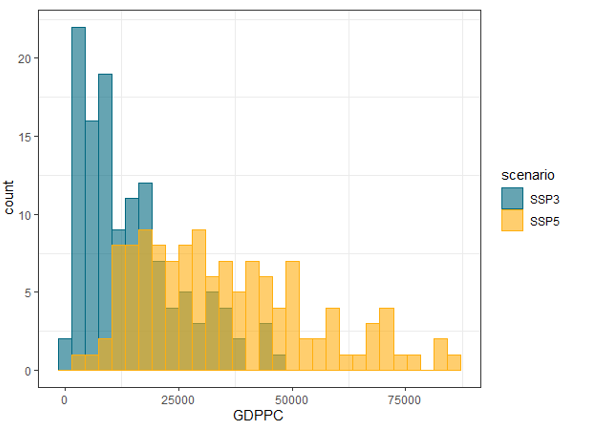

We’re particularly interested in progress of lower-income countries. For the 140 countries that are currently eligible for aid (official development assistance), the scenarios are more optimistic—especially when compared to historical experience (light grey bar) but the variance is higher between scenarios. Under SSP5, the median growth among these countries is projected to be 5.7 percent (amounting to a five-fold increase by 2050) and under SSP3, it is projected to be 2.2 percent (GDP per capita would roughly double). Figure 2 shows the distribution of GDP per capita among today’s ODA-eligible countries in 2050, according to SSP3 and SSP5.

Figure 2. Distribution of incomes among today’s ODA-eligible countries in 2050, SSP3 and SSP5

Notes: Data are not weighted for population

Each scenario is more optimistic about growth in ODA-eligible countries than the historical experience of the past 30 years (potential measurement issues aside). Perhaps we should be confident that growth will improve for this group, but the fact that none of the scenarios envision growth lower than recent historical experience puts a question mark on their breadth. Since the IPCC's scenarios are already important to expectations of countries' future greenhouse gas emissions, and shaping policies to curtail them, this suggest that even the most-pessimistic scenario may be too high. Further work on longer-term projections for this group specifically—including many countries often neglected by forecasters as demonstrated in table 1—may be warranted.

Common implications of the SSPs

The SSPs imply radically different futures. This could mean the difference between the majority of the world’s population enjoying living standards similar to that in today’s wealthy countries, and continued poverty alongside lower resilience to the shocks that will become ever more common as the climate changes. However, there are some implications common to each scenario. This doesn’t mean make them inevitable, but given that the SSPs were chosen to portray a wide range of scenarios, it means they should be taken seriously.

1. The end of low-income countries (LICs)?

There are currently 30 countries categorised as LICs according to the World Bank (those with income per head below $1,035, that we estimate to be equivalent to $2,919 in 2017 purchasing power parity terms). The number of LICs has been steadily declining over time, and even under the most pessimistic scenario this is set to continue, with the number projected to halve by 2050. Two SSPs even anticipate there being only one LIC (Somalia) by this year(though this seems implausible based on history). While the decline in LICs would be a positive story, it also calls into question appropriateness of certain funding models. In particular, the funding decisions of institutions like the Global Fund and the World Bank’s IDA fund depend on whether or not a country is a LIC, and would therefore need to alter their aims and/ or funding models with so few countries eligible.

2. Will providers of development finance outnumber recipients?

Equally, the number of countries who might step up when it comes to development finance will increase. Back in 1960-61 when aid providers formed the Development Assistance Committee (then the Development Assistance Group (DAG) the average GDP per capita among the ten members was around $12,500 (in 2017 prices). Under SSP3—again, the least optimistic—the number of countries above that level rise from 88 in 2020, to 118 in 2050, over half the countries in the world. Many of these countries are already providers of development assistance in the form of south-south cooperation. And clearly the relative income of countries matters too, especially if potential new providers feel that richer countries never kept promises, either on giving 0.7 percent of Gross National Income as ODA, or meeting the $100 billion climate finance target. Nevertheless, the balance between countries likely to be net providers, and net receivers, is going to shift, even in the most pessimistic scenario.

3. Is regional inequality with us for foreseeable future?

While all the scenarios suggest that by 2050 there will be some dent in regional inequalities, it will not be significant in any of them. Sub-Saharan Africa’s share of global GDP would be highest under SSP5, at 7 percent (up from around 3 percent today), but this would still be for a region with nearly a fifth of the global population. Under SSP4, the figure would only be 4 percent.

In other words, none of the SSPs anticipate fast enough convergence for the global distribution of economic power to change dramatically in the next few decades. This probably also suggests that Africa’s contribution to global emissions will also remain small.

Is a better guide for the future of development possible?

All forecasts are wrong, and none of the SSPs will be realised. But our analysis suggests they are the only serious attempt to look at long-term future economic growth of lower income countries.

However, they seem far too optimistic by historic standards. By design, they also exclude the impact that climate change might have on growth, which could be substantial, especially for poorer countries. And while they are intended to cover a range of outcomes, some projections look fanciful (the Democratic Republic of Congo’s GDP is projected to be 30 times bigger by 2050 according to SSP5). But the SSPs provide a starting point on the implications for how development efforts and finance might be resourced and focussed in the coming decades .

In future publications we will take a closer look at long-term economic growth scenarios, the SSPs and their plausibility, and explore how (or whether) they should change the way we think about the future of development. If you’re aware of work in this area please get in touch.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.