Recommended

The COVID-19 pandemic has cost lives and disrupted economic activity worldwide. It has impacted government budgets globally by reducing tax receipts and increasing spending on programs to save lives and transfer income to those adversely affected by the pandemic. Does the budgetary impact vary across advanced and developing countries and depending on which budget component is affected more? And if the budget impact is significant, what is the possibility of developing countries implementing tax reforms to mitigate the negative effect of the pandemic? Today we publish that seeks to answer these two interlinked questions.

Does the budgetary impact vary across advanced and developing countries and depending on which budget component is affected more? And if the budget impact is significant, what is the possibility of developing countries implementing tax reforms to mitigate the negative effect of the pandemic?

Budgetary impact of pandemics

Although COVID-19 stands out as a “once-in-a-century” crisis for the severity of its health and economic impacts, other pandemics and epidemics in the past 20 years offer insight into the fiscal impact of these events and how countries may, or may not, undertake fiscal reforms in response.

We first examined the short- to medium-term budgetary impact of past pandemics—including SARS, N1H1, MERS, Ebola, and Zika—in a sample of 170 countries, including developing ones. We find that the budgetary impact is substantial in all countries. However, in the case of developing countries, the negative toll pandemics have on the budget is long-lasting, largely because of a significant fall in revenues (see figures 1 and 2). This contrasts with advanced economies, where revenues are not affected as much but expenditures increase owing to the natural operation of automatic stabilizers, which are larger in this group of countries. Automatic stabilizers are mechanism built into budgets that increase spending (e.g., on unemployment benefits) or lower taxes when the economy slows.

Figure 1. Impact of pandemics on total expenditures (% GDP)

Note: Impulse response functions are estimated using a sample of 170 countries over the period 1980-2017. The graph shows the response and both the 90 and 68 percent confidence bands. The x-axis shows years (k) after pandemic events; t = 0 is the year of the pandemic event. Estimates based on equation 1. Standard errors in parentheses are clustered at the country level.

Figure 2. Impact of pandemics on total revenues (% GDP)

Note: See previous note.

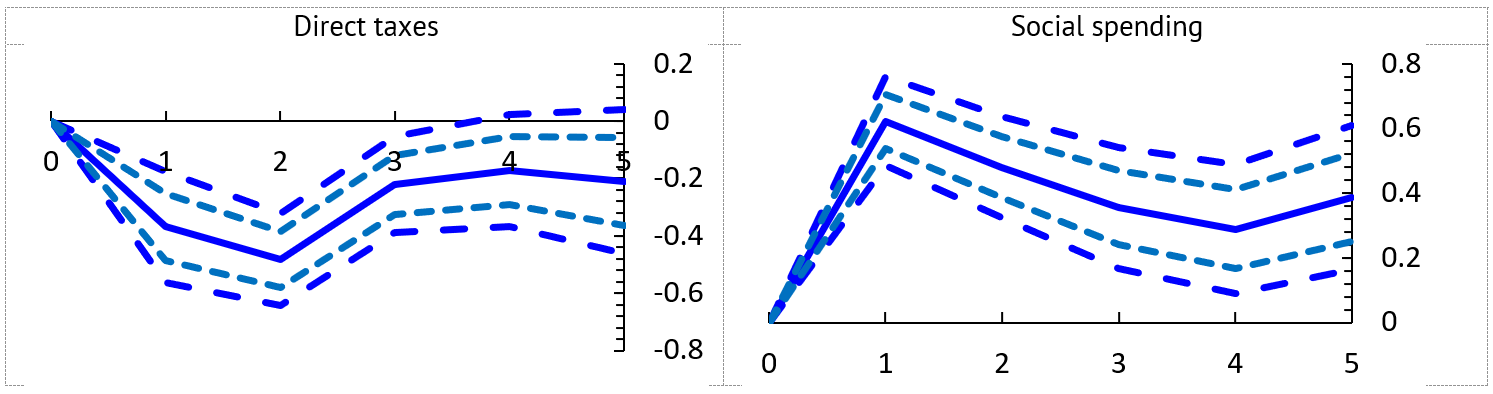

A relevant question is whether the effect on the budget is being driven by a particular component of revenues and expenditure. To answer this, we separate revenues into direct taxes (e.g., income and corporate taxes), indirect taxes (e.g., the value-added tax), and non-tax revenues (e.g., external grants). We separate expenditures into public consumption, public investment, and social spending. We find that the fall in revenue is mostly driven by a drop in direct taxes followed by a decline in non-tax revenues. Expenditure increase, in turn, is mostly the result of the operation of automatic stabilizers arising from higher spending on social programs (Figure 3).Note: See previous note.

Figure 3. Impact of pandemics on key revenue and expenditure components (% GDP)

Note: See previous note.

Pandemics and tax reforms

As many developing countries have limited fiscal space to accommodate the shock arising from the pandemic, we further examined whether the COVID-19 pandemic would create conditions for them to implement much-needed tax reforms to raise revenues over the longer term. For this purpose, we relied on tax reform data from 45 emerging and low-income countries over the 2000–2015 period. Our results indicate that past pandemics created conditions for countries to implement tax reforms, particularly in corporate income taxes, excises, and property taxation.

Unfortunately, while pandemic seem to trigger some tax policy reforms, they do not drive developing countries to implement revenue administration reforms. Across revenue administration areas such as management of human resources, registration and filing, and audit and verification, past pandemic events have not led to significant reform.

What does this mean for low-income developing countries?

The above results have important implications for low-income developing countries, where average tax-to-GDP ratio is around 15 percent, and in many instances lower than the level necessary to achieve a significant acceleration in growth and development. The COVID-19 pandemic will significantly affect the tax bases of these countries for several years. This means that policymakers in these countries would need to reconsider their revenue-raising strategies in favor of an approach that embraces a comprehensive reform package, including policies that have encountered political resistance and opposition in the past. The good news is that pandemics can propel these countries into implementing tax reforms in certain key areas.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.