Recommended

CGD NOTE

Valuing Climate Liability

While a drastic reduction in carbon emissions is necessary to contain climate change, countries still have not reached a consensus on a fair division of responsibilities in reducing them. While advanced economies were the biggest emitters in the past, emerging economies, such as China and India, account for an increasing share of new emissions, fueled in part by high rates of economic growth. From the standpoint of fiscal policy, these carbon emissions, which adversely affect the world’s well-being, are a negative externality—that is, a cost imposed by consumption of certain forms of energy and goods by a country on the entire globe. At present, countries do not bear the full cost of these externalities. The cumulative sum of these liabilities can be viewed as a “climate debt” a country owes to the global community.

Mitchell, Robinson, and Tahmasebi have conservatively estimated climate liabilities over the 1989-2018 period at a carbon price of $50 per ton of CO2 emissions (at 2015 prices) in 2030. This estimate was the lower bound of the of estimates prepared by the high-level commission chaired by Stiglitz and Stern. The value of these liabilities for China and the US exceeds $5 trillion each, constituting roughly 40 percent of the global total. Mitchell et al. made a simplifying assumption in their estimates that until the establishment of Intergovernmental Panel on Climate Change in 1989, the world was not fully aware of the costs associated with global warming.

Given the modest steps taken thus far by countries to meet their commitments for emissions reductions, there is good reason to believe that climate debt will continue to rise in coming years. Building on the work of Mitchell et al., we estimate climate debt for G20 countries from 2019 to 2035, and find that it will rise by a staggering $57 trillion in 2035, an average increase of 85 percent of GDP. Along with rising pensions and health liabilities, this will hamstring policy choices and could result in sub-optimal social outcomes. What has made the situation worse is the advent of the COVID-19 pandemic, which has severely impacted the fiscal situation of countries, leading to unprecedented increases in fiscal deficits and public debt ratios in 2020 (IMF, 2021).

Measuring climate debt 2019-2030

Estimates on the social cost of carbon (SCC) vary widely, although climate models generally indicate that the damages from emissions rise over time. Since Mitchell et al. estimates were prepared, Stiglitz and Stern have argued in favor of the upper end of SCC estimates by the high-level commission ($100 per ton of C02 emissions by 2030). Accordingly, we base our forward-looking estimates on the higher price. For the years prior to 2030, we assume that SCC changes by 3 percent annually in real terms, as argued by IMF staff (Coady et al., 2019).

Annual data on carbon emissions until 2018 are available in Ritchie and Rosen (2017). They include C02 emissions from both burning of fossil fuels and those arising from cement production. We estimate the growth rate of emissions on the basis of projections for all greenhouse gas emissions from the IMF’s Fiscal Affairs Department, which follow the methodology described in the IMF’s Fiscal Monitor (2019). These projections incorporate the reduction in emissions observed in 2020. For example, for the United States, greenhouse gas emissions fell by 12 percent last year. The forecast represents a baseline in which countries do not implement new measures to meet their carbon emissions targets, and thus should be interpreted as a “no policy change” scenario. On this basis, we present both forward looking estimates of SCC of emissions as well as for 1989-2018 (Table). Baseline estimates for other fiscal liabilities are derived on the basis of IMF data.

Table. Cumulative climate debt and fiscal indicators (Percent of GDP), G20 countries

| Climate debt, 1989-2018/GDP in 2018 | General Government Gross Debt 2018 | Climate debt projection (no action scenario), 2019-2035/ GDP in 2018 | NPV of pension spending change, 2019-20351 | NPV of health care spending change, 2019-20352 | |

|---|---|---|---|---|---|

| Argentina | 47.5 | 41.5 | 63.0 | N/A | N/A |

| Australia | 39.0 | 86.1 | 54.1 | 8.0 | 13.6 |

| Brazil | 29.2 | 87.1 | 43.1 | 47.7 | 9.1 |

| Canada | 47.9 | 89.7 | 55.7 | 10.2 | 13.6 |

| China | 69.9 | 49.1 | 169.1 | 28.4 | 8.0 |

| France | 20.8 | 98.4 | 23.7 | 4.5 | 13.6 |

| Germany | 32.7 | 61.9 | 33.8 | 13.6 | 8.0 |

| India | 82.7 | 69.4 | 251.3 | 9.1 | 2.3 |

| Indonesia | 53.7 | 29.4 | 120.9 | 2.3 | 2.3 |

| Italy | 30.3 | 134.8 | 26.7 | 19.3 | 9.1 |

| Japan | 37.2 | 236.5 | 39.4 | -14.8 | 21.6 |

| Korea | 42.4 | 37.9 | 70.8 | 20.5 | 23.9 |

| Mexico | 53.4 | 53.7 | 64.9 | 5.7 | 5.7 |

| Russia | 148.7 | 13.6 | 200.8 | 35.2 | 5.7 |

| Saudi Arabia | 80.6 | 19 | 140.9 | 21.6 | 5.7 |

| South Africa | 171.8 | 56.7 | 230.2 | 3.4 | 5.7 |

| Turkey | 54.8 | 30.4 | 122.5 | 3.4 | 8.0 |

| United Kingdom | 26.9 | 85.7 | 22.3 | 3.4 | 14.8 |

| United States | 40.6 | 106.9 | 43.6 | 12.5 | 56.8 |

Sources: Authors’ calculations using CO2 historical emission data from Ritchie and Roser (2017); emissions projections from the IMF’s Fiscal Affairs Department; and the IMF Fiscal Monitor, October 2020.

Notes: 1,2 NPV of pension and health care spending increases are estimated based on projected increases in spending from 2019 to 2030 from the IMF Fiscal Monitor. A discount rate for future increases as a share of GDP of 1 percent per year is used.

Figure 1 provides an estimate of the climate debt accumulated over 1989-2018 in the G20. Consistent with Mitchell et. al. estimates, China and the United States stand out as the major contributors, accounting for over half of the accumulated climate debt. The accumulated climate debt from 1989-2018 is sizeable in most G20 countries, averaging about 50 percent of GDP—about five-ninths of their ratio of public debt to GDP.

Figure 1. Cumulative climate debt (billions), 1989-2018, G20 countries

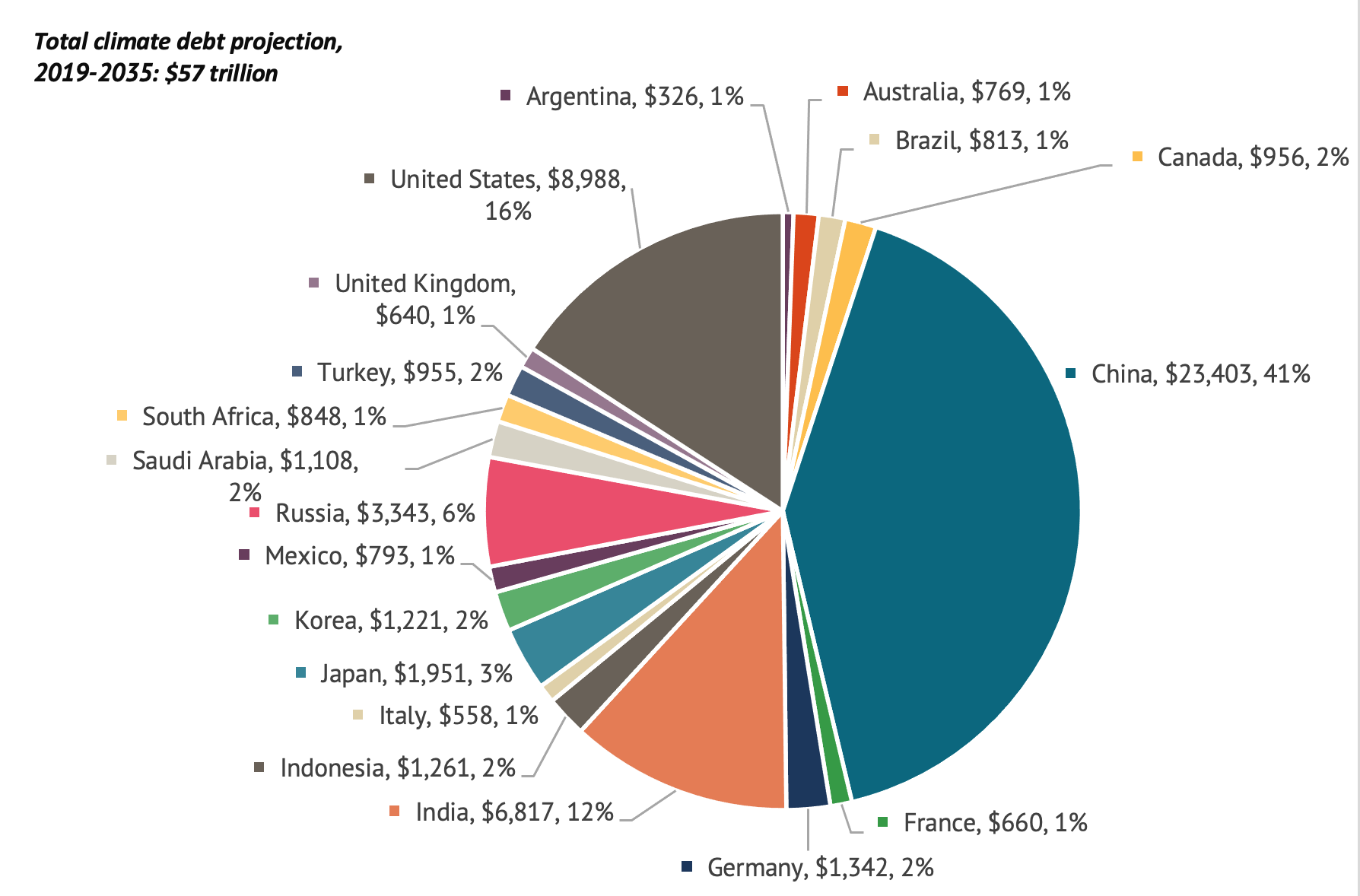

What is striking is the very large increase in climate debt that will be racked up over the next 17 years under the no policy change scenario. In absolute terms, climate debt would rise to $57 trillion dollars—an increase of two-thirds relative to that accumulated over the previous 30 years. Both China and the United States will continue to account for a large share of the new climate debt (Figure 2), but China will account for an increasing share, rising to 41 percent of the G20 total. India’s share will rise from 7 percent to 13 percent of the total. Of course, actual outcomes are likely to be lower, as increasingly countries are committing to lowering carbon emissions in the future. For example, China has declared that it would make its economy carbon neutral by 2060.

Figure 2. Climate debt projection (billions), 2019-2035 (no action scenario), G20 countries

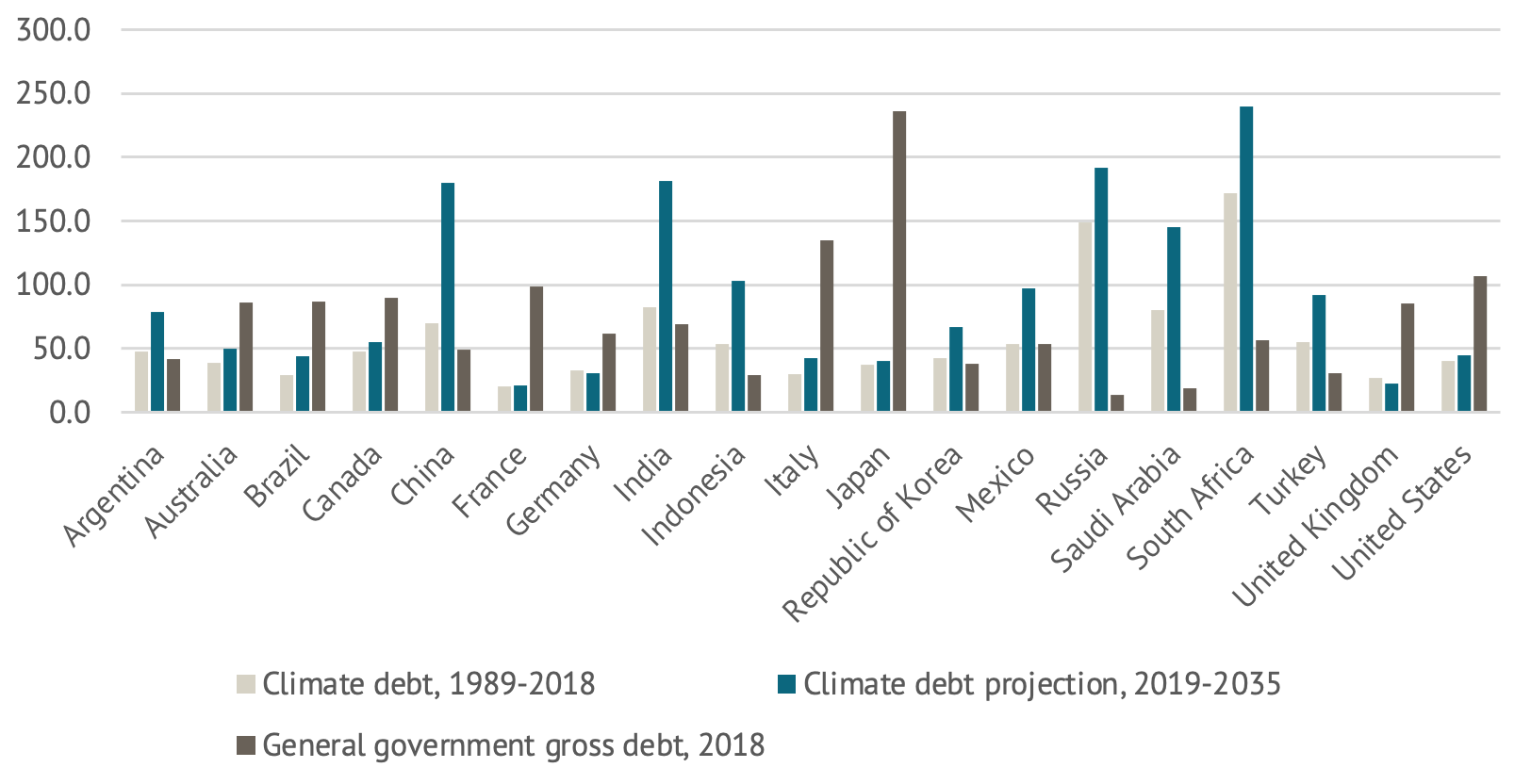

In the absence of policy action, an average G20 country would accumulate an additional climate debt of 85 percent of GDP. The greatest increases (relative to their GDPs) would take place in China, India, Russia, and South Africa, while the smallest will be in France, Germany, Italy, and the United Kingdom (Figure 3).

Figure 3. Climate debt and public debt (Percent of GDP), 2019-2035, G20 countries

Fiscal policies to reduce climate debt

Reducing the accumulation of climate debt will be a steep challenge for most G20 countries. This is in part because public debt ratios in all countries have risen since 2018. In the advanced G20 economies, for example, it rose by an average of 20 percent of GDP in 2020. On top of higher public debt, countries must also confront the rising costs of pensions and public health care, which will experience cumulative increases in spending of about 25 percent of GDP in NPV terms over the next 17 years—about a third of their public debt in 2018. These estimates do not account for the impact of COVID-19 on health spending in future years. An important implication of fiscal pressures is that there may be limited room for new expenditures (such as green infrastructure) to reduce the growth of climate debt, once countries begin to focus, over the medium term, on fiscal consolidation.

What is the alternative? Countries could turn to the revenue side, in particular greater taxation of energy with carbon taxes. Taxation would have the advantage of reducing emissions while also helping countries to fund spending on green infrastructure.

Carbon taxation will need to be accompanied by complementary fiscal policies to offset their burden on low-income households. In developing economies, carbon taxation is generally found to be progressive, hitting upper-income groups more than others (Dorband et al., 2019). Nonetheless, to garner political support for reforms, lower and middle-income groups will need to be compensated for higher energy costs. In advanced economies, energy taxes can be regressive. Policies that recycle some of these carbon revenues for well targeted spending, however, can lead to a policy package that, as a whole, reduces inequality (IMF, 2019).

In sum, the climate debt accumulated over the past 30 years is large and is projected to rise by another two-thirds in just the next 17 years. This underscores the urgency of policy action to help slow these increases. Greater taxation of carbon provides the best way forward to achieve the twin goals of limiting climate change and maintaining fiscal sustainability.

Benedict Clements is a professor at the Universidad de las Américas, Quito, Ecuador.

We would like to thank Ian Mitchell and Lee Robinson for helpful comments on an earlier draft.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.