Summary

The IMF should set up a Global Resilience Trust (GRT) without delay, allowing at least $50 billion from the recent special drawing rights (SDR) allocation to be channeled to low- and middle-income countries. The urgent purpose is to meet the challenges of climate change, reduced biodiversity, and desertification through mitigation and adaptation. Success of this initiative depends, however, on following a particular design that will carefully address the many demands, expectations, and restrictions placed upon use of these funds, as well as the imperative that it fits well into a much larger quilt of international cooperation.

In an earlier note, we explained the elements needed for the GRT to meet these various constraints. The present note considers in detail the elements of a GRT that the IMF staff will have to consider in its design. Following in the footsteps of the Poverty Reduction and Growth Trust (PRGT), the new GRT can deal with many legal and policy constraints while establishing its own identity. In particular, the proposal:

-

maintains the reserve asset nature of SDRs.

-

can be established quickly, with a proven governance structure.

-

includes a policy framework designed to satisfy creditors while being attractive to borrowers. The GRT would be neither too easy to access, nor too hard.

-

envisages broader initiatives in international cooperation to enable the GRT to be fully effective by fostering policy coherence and leveraging resources. In doing so it sees a role for many institutions and the private sector in helping to build resilient economies.

Time is very short to establish this Trust while the opportunity arises from the recent SDR allocation and the need for governments at COP26 to produce new initiatives:

-

At the G20 and IMF-World Bank Annual Meetings in October, the IMF should be tasked to (a) establish the Trust; and (b) develop a pilot for National Resilience Plans (NRPs) and assessments of them to be used in Article IV discussions and requests for access to the Trust; and creditor governments should (c) provide initial pledges for the rechanneling of SDRs to meet the $50 billion minimum, together with related subsidy and reserve fund resources.

-

At COP 26 in November, governments should (a) finalize their pledges to fully fund the Trust; and (b) volunteer to be one of at least 20 countries—representing a variety of circumstances and income levels—willing to participate in the pilot scheme to present and discuss their NRPs in annual consultations with the IMF. In addition, this would be the occasion to (c) announce several eligible countries about to step forward to present their NRP and request support from the Trust; and (d) plan the first of a series of resilience financing conferences at which private sector investors and official creditors and donors would be invited to support the first batch of GRT recipients.

As chairs, the UK and Italy have key roles in lining up volunteers and pledges. As other institutions pursue complementary initiatives, the IMF can play a leadership role in establishing the new Global Resilience Trust.

Overview

The IMF should set up a Global Resilience Trust (GRT) without delay, allowing at least $50 billion from the recent special drawing rights (SDR) allocation to be channeled to low- and middle-income countries. The urgent purpose is to meet the challenges of climate change, reduced biodiversity, and desertification through mitigation and adaptation. Success of this initiative depends, however, on following a particular design that will carefully address the many demands, expectations, and restrictions placed upon use of these funds.

Momentum is increasing for the IMF to establish a new financial facility that will support countries’ efforts to accelerate the green transition and build more resilient and sustainable economies.[1] A new Global Resilience Trust would allow the IMF to play its part in a much broader initiative in international cooperation—involving many players—that is both necessary and urgent.

The international community should seize the opportunities provided by the recent injection of global liquidity thorough the allocation of the IMF’s SDRs and by the imperative for new initiatives to tackle climate change, notably in the context of this November’s COP26 meeting.

Threading the needle to get a GRT up and running is clearly possible if there is the political will to do so. Time is of the essence, but for this ambition to be realized the IMF will first need to navigate many legal, policy, and political hurdles. In this note we set out a way to do so.

This note (i) outlines the proposal; (ii) explains how such a Trust successfully addresses various constraints imposed by the G7 and others in a way that can make the proposal attractive to borrowers and acceptable to creditors; and (iii) sets out a series of actions to deliver a Trust by the end of the year.

Outline of a new IMF Global Resilience Trust

The basic elements of the design are straightforward:

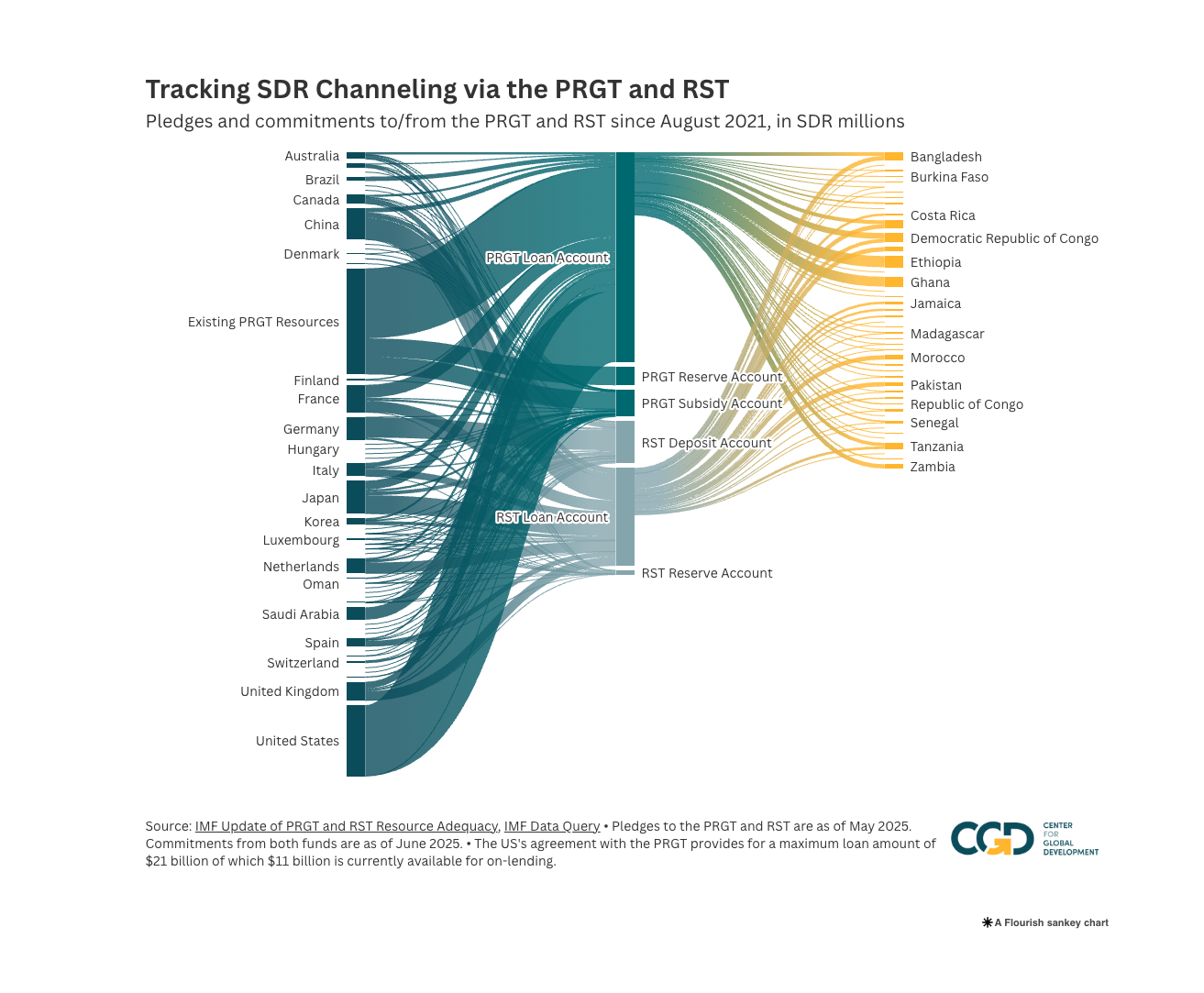

The IMF would establish a new Global Resilience Trust (GRT), similar in structure to the existing Poverty Reduction and Growth Trust (PRGT) that it already manages. The main sources of funds would be at least $50 billion worth of SDRs lent by advanced countries who agree to rechannel part of their allocation of the $650 billion of SDRs made available by the IMF in August 2021.[2] The main recipients of the loans from the GRT would be low- and middle-income countries in support of policy actions to make their economies more resilient by adapting them in specific ways.

The IMF Executive Board would have a central role in program design. It would:

-

decide the eligibility requirements. We would suggest broad coverage of low- and middle- income countries.

-

establish the terms of loans granted under the trust. In our view, to support a three-year policy program with long-term impact the maximum loan period could be longer—say, fifteen years—than the ten years for PRGT loans. Low-income countries would qualify for concessional (essentially zero-interest) terms. Access to GRT loans would be additional to that permitted under other IMF facilities.

-

establish the policy framework for the new Trust.

-

approve individual requests from qualifying countries for financial support.

Key elements of the needed policy framework

The policy framework is the most critical element in ensuring support for the GRT and its eventual success in helping countries face the economic transition ahead. Four aspects merit close consideration: the concept of resilience that is targeted; the nature of the balance of payments need associated with achieving that resilience; the policies a country would be expected to pursue to achieve the program’s resilience goals over the length of the loan; and the integration of this IMF facility into the much broader fabric of international cooperation, involving the World Bank and other multilateral development banks (MDBs), the various UN frameworks, national governments, civil society, and the private sector, as well as the IMF’s existing responsibilities. We consider each of these four elements in turn.

The resilience objective refers to a country’s ability to absorb several anticipated shocks to a country’s balance of payments, macroeconomic stability, and prosperity that arise from the successes or failures of the global “green transition.” Whether over the next quarter century the global efforts at mitigation succeed or fail, the impact on all economies will be profound and, in the case of failure, potentially catastrophic. For many low- and middle- income countries the impact will be exacerbated by the need for radical economic restructuring with limited access to the means to finance it, while at the same time these countries pursue the prosperity that their populations have so far been denied. Each country will need to adapt to deal with the implications of (a) implementing its own commitments to mitigate climate change, maintain biodiversity, and prevent desertification;[3] (b) the spillover of the rest-of-the-world’s policies to mitigate and adapt; and (c) the climate change, reduced biodiversity, and desertification that will now occur despite the declarations of global ambition for mitigation.[4]

The balance of payments need—a particular requirement for all IMF lending—could materialize in different ways. It might result from a country’s own mitigation policies—for example, reducing fossil fuel production or carbon and methane emissions, limiting tourism in areas threatened by diminishing biodiversity, protecting forests and fisheries, spending more on relevant public investment, or restructuring debt from stranded assets.[5] Alternatively, the balance of payments need could arise when the country faces or anticipates the direct consequence of the actions or inactions of the rest of the world (for example, a loss of export markets if carbon border taxes or regulations are imposed, or increased food insecurity if crop yields and fish stocks diminish) as well as the consequences of the country’s own attempts to adapt to such changes (for example, expenditures to relocate population affected by rising sea levels, or to invest in human and physical capital to spur new industries).

The policies supported by the trust would include actions taken now—or over the program period—to mitigate or adapt to climate change, reduced biodiversity, and desertification. At the same time the related balance of payments need would be addressed by increased financing and eventually as the policies aimed at restructuring the economy and its finances take effect. Policies would vary widely by country circumstance, reflecting the different ways in which economies will be restructured to meet future global conditions and domestic energy demand consistent with growth and development. Emphasis would be placed on signaling the direction and establishing the structure of relative prices (including the price of carbon) that would give the incentives to change behavior of consumers, producers, and investors; regulations and supervision, including over the banking sector; and restructuring of the public finances, including relevant public sector capital and current expenditures, and domestic revenue mobilization. A key policy element would be the redistribution of any increased revenue from emissions-based taxes to those whose real income is most affected. The conditions for IMF lending would aim to maintain a sound macroeconomic framework, gain domestic support, and give confidence to investors; they would focus on measures that the IMF could analyze and monitor adequately and that could achieve the program objectives.[6]

The broader fabric of international cooperation would be substantially strengthened. To be fully effective, the Trust should be seen in the broader context of international cooperation provided by other IMF responsibilities and those of other institutions, including the World Bank and MDBs. In particular, global resilience involves all IMF member countries, not just those eligible for access to the Trust, especially since the world’s largest economies will be responsible for the largest contribution to global mitigation efforts and will be the source of most public and private financing for global resilience. In this context we propose several initiatives:

-

First, each country—from the largest to the smallest—prepare a National Resilience Plan (NRP) outlining the anticipated macroeconomic impact of climate change, reduced biodiversity, and desertification, and of the policy response to them, including mitigation and adaptation policy actions and intentions (incorporating its nationally determined contribution (NDC) to decarbonization and its National Adaptation Plan (NAP) provided under the UN Framework Convention on Climate Change). This process should facilitate convening multiple government ministries and applying a consistent whole-of-government approach. The NRP would be discussed in the context of the annual consultation discussions on economic policies held with the IMF, and would be published, along with the reaction to it. Those countries requesting access to the GRT would use the NRP as the basis for their policy program. The IMF’s unique global reach would enable it to analyze the aggregate consistency of countries’ NRPs, and better understand the spillovers affecting other countries, including those eligible for Trust resources.

-

Second, the NRPs would incorporate the macroeconomic policy implications and impact of any parallel initiatives of the World Bank and other MDBs with low-income and middle-income countries, especially the implications of the restructuring and refinancing of particular sectors. Over time, enhanced cooperation could yield more in-depth joint assessments for some countries, analogous to the Fund-Bank Financial Sector Assessment Program (FSAP) established in the wake of the Asian financial crisis.

-

Third, a new series of resilience financing conferences (of donors and private investors) would be convened by the IMF and World Bank, at which countries would present their NRP and describe the policies undertaken and supported by a GRT loan and any associated arrangements with the Bank and other MDBs. Assessments of the IMF and Bank staff could also inform debt restructuring fora where relevant. These conferences would provide the opportunity for creditor countries to augment their support for low- and middle- income countries, including potentially by further SDR rechanneling.[7]

These initiatives should ensure that the IMF financing through the GRT plays a catalytic role in meeting the financing needs of member countries; improves the global surveillance of the macroeconomic policies for resilience; and increases the transparency of efforts at mitigation and adaptation that should assist civil society in its advocacy as well as consumers, producers, and investors as they adjust to new economic incentives.

How this model satisfies various concerns and constraints

The proposed approach untangles many of the complex legal, policy and political knots that could otherwise derail the deceptively simple desire to “rechannel SDRs” to support countries’ policies to build resilience. By doing so it conveys several advantages over other possible models.

First, it maintains the reserve asset nature of SDRs. The trust can be structured to meet the requirement of many creditors who wish to use what is essentially a reserve asset for long-term lending that involves both liquidity and credit risk. Replicating the structure of the PRGT, which faced analogous issues in facilitating the intermediation of reserve assets for long-term lending, the new GRT would comprise three elements—a loan account, a subsidy account to the extent that concessional lending is envisaged,[8] and a reserve account to cover the potential credit risk if loans were not repaid.[9] In addition, as with the PRGT, an encashment scheme would be put in place to counter liquidity risk if a creditor needed to recall its SDR loans at short notice. In addition to the SDR loans, creditors and donors would need to contribute hard currency resources for the subsidy and reserve accounts.[10]

Second, it can be established quickly, with a proven governance structure. Approval of the GRT itself would not require a special majority vote in the IMF’s Executive Board.[11] It would, however, require very broad support to ensure adequate financial backing, both SDRs to on-lend and donations for the subsidy and reserve accounts.[12] The governance structure already exists (and is tried and tested for the similar PRGT) to take necessary decisions to set up the trust and define its policy framework. The conditionality, safeguards, and publication policies give confidence in the transparency of the trust’s operations and provide further help to reduce credit risk. There is also an established framework for program negotiation, presentation to the Board, links to other IMF activities and leveraging other funding.

Third, its design can deal with conflicting concerns: that the trust would be too easy to access, or too hard. On the one hand, creditors may be reticent to provide funds for the Trust if they are concerned that countries could access loans too easily and avoid “regular” IMF programs to tackle traditional balance of payments needs—the so-called “facility shopping” problem. On the other hand, potential borrowers could refrain from requesting support from the Trust if it carried the stigma of a traditional IMF program—for example if the conditions for support were seen as too stringent. How can a balance be struck?

-

Several features make the GRT attractive to borrowers. Requesting assistance to build resilience is a positive motivation that should not involve the same stigma as requesting IMF financial support to overcome policy-induced balance of payments problems. The Trust could be accessed on its own by countries with a sound macroeconomic position and no immediate balance of payments difficulty other than that induced by the policy measures to build resilience. (Countries with other balance of payments needs could simultaneously request access to regular IMF facilities as well as the GRT and undertake policies relevant to both.) The policy conditions for the GRT would usually be limited to several key aspects of pricing, public finance and regulations that are part of a country’s own NRP to meet their mitigation and adaptation objectives. The terms are favorable, with a lengthy repayment period and low or essentially zero interest rate. Moreover, the catalytic role of the GRT financing is key, with the opportunity for a country to present its program to broader international fora to encourage additional financing and debt relief initiatives from other official creditors and the private sector investors who will provide the bulk of the financing for the energy transition. GRT loans would also be additional to any support, if requested, from other IMF facilities.

-

The GRT policy framework should also make it acceptable to creditors. The GRT policy framework ensures that the combination of objectives, time horizon, balance of payments need, and policies is sufficiently distinct from those under regular facilities, including the IMF’s General Resources Account (GRA) and the PRGT, to prevent “facility-shopping.” If other types of balance of payments need are evident, for example caused by expansive fiscal policy not related to climate change mitigation or adaptation, the country should request support from regular IMF facilities and adopt policies to address that issue. Creditors would also be assured by the policies in place to lower credit risk, including the IMF’s safeguards assessments and the transparent monitoring of policy adherence.

Fourth, this proposal sees a role for many institutions and the private sector in helping to build resilient economies and should therefore reassure those who resist too large an IMF role. The IMF-based contribution—with a relatively limited amount of money—is just one part of a much larger international effort and focuses on the macroeconomic policies and implications of measures to build resilience that are the IMF’s responsibility. The magnitude of the global challenge means that all institutions must play their part. The IMF’s ability to catalyze resources far larger than the amounts it would disburse under the GRT involves cooperation with other institutions, including the World Bank and other MDBs and donors; as well as tapping into the huge potential impact of private finance through its signaling of policy direction.

Next steps: deliverables in 2021

Time is very short to establish this Trust while the opportunity arises from the recent SDR allocation and the need for governments at COP26 to produce new initiatives:

-

At the G20 and IMF-World Bank Annual Meetings in October, the IMF should be tasked to (a) establish the Trust, and (b) develop a pilot for the National Resilience Plan and its assessment to be used in Article IV discussions and requests for access to the Trust; and governments should (c) provide initial pledges for the rechanneling of SDRs to meet the $50 billion minimum, together with related subsidy and reserve fund resources.

-

At COP 26 in November, governments should (a) finalize their pledges to fully fund the Trust; and (b) volunteer to be one of at least 20 countries—representing a variety of circumstances and income level—willing to participate in the pilot scheme to present and discuss their NRPs in annual consultations with the IMF. This would also be the occasion to (c) announce several eligible countries about to step forward to present their NRP and request support from the Trust; (d) announce the first of series of resilience financing conferences at which private sector investors and official creditors and donors would be invited to support the first batch of GRT recipients.

As chairs, the UK and Italy have key roles in lining up volunteers and pledges. As other institutions pursue complementary initiatives, the IMF can play a leadership role in threading the needle to make the new Global Resilience Trust a reality.

The author is grateful to Masood Ahmed, David Andrews, Sean Hagan, Claire Healy, Kathryn McPhail, Mark Plant, and members of a CGD technical working group on SDRs, for helpful discussions. All errors are the author’s alone.

References

-

“Remarks by IMF Managing Director on Global Policies and Climate Change at the International Conference on Climate, Venice,” July 11, 2021.

-

Andrews, David, John Hicklin and Mark Plant, “Three Ways New SDRs Can Support the IMF’s Lending to Low-Income Countries,” Blog Post, Center for Global Development, April 29, 2021.

-

Hicklin, John, “A New IMF Facility to Support the Green Transition?” by, Blog Post, Center for Global Development, April 29, 2021.

-

Plant, Mark, John Hicklin, and David Andrews, “Reallocating SDRs into an IMF Global Resilience Trust,” Note, Center for Global Development, September 23, 2021.

-

Rajan, Raghuram, “A Global Incentive To Reduce Emissions,” Project Syndicate, May 31, 2021.

-

Truman, Edwin M., “Does the Special Drawing Right Have a Future?” forthcoming.

-

Wolf, Martin, “A windfall for poor countries is within reach,” Financial Times, June 1, 2021

[1] The IMF foreshadowed a Resilience and Sustainability Trust, as did reporting in the Financial Times (“Remarks by IMF Managing Director on Global Policies and Climate Change at the International Conference on Climate, Venice,” by Kristalina Georgieva, July 11, 2021 and “A windfall for poor countries is within reach,” by Martin Wolf, Financial Times, June 1, 2021). We have previously outlined the case for a new IMF facility for the green transition (“A New IMF Facility to Support the Green Transition?” by John Hicklin, Blog Post, Center for Global Development, April 29, 2021) and the elements needed for the Global Resilience Trust to meet various constraints (“Reallocating SDRs into an IMF Global Resilience Trust,” By Mark Plant, John Hicklin, and David Andrews, Note, Center for Global Development, September 23, 2021).

[2] Though rechanneled SDRs would be the main source of funds, other bilateral loan agreements could also be included.

3. Mitigation policies of the poorest countries often have minimal global impact (reduced carbon emissions, for example) but could still be justified if other benefits accrue such as improved health outcomes. Moreover, mitigation may be part and parcel of the need to adapt to more stringent requirements for export industries.

[4] In principle, the concept of resilience for the GRT could be widened to include pandemic preparation though we focus on those aspects of resilience best suited to the IMF’s macroeconomic policy expertise.

[5] In the case of the PRGT, the policies to reduce poverty and increase growth were assumed to create or exacerbate the balance of payments need. Similar arguments could be developed for the new trust.

[6] This may require the IMF staff to acquire new skills and tools to assess the resiliency impact of climate-related and other actions.

[7] The historical debate on the use of SDRs for development objectives is described in “Does the Special Drawing Right Have a Future?” by Edwin Truman (forthcoming). Augmented SDR (or hard currency) rechanneling from developed to developing countries could be based on the elegant scheme for redistributing resources proposed by Raghuram Rajan in “A Global Incentive To Reduce Emissions,” Project Syndicate, May 31, 2021.

[8] Subsidies would not be required if creditors are willing to lend SDRs at the same concessional rate that borrowers would pay.

[9] For further details, see “Three Ways New SDRs Can Support the IMF’s Lending to Low-Income Countries,” by David Andrews, John Hicklin and Mark Plant, Blog Post, Center for Global Development, April 29, 2021.

[10] Given the global public good aspect of the GRT, it would be reasonable that at least the administrative costs of the new Trust be borne by the IMF itself, rather than the new reserve account as had been the case with the PRGT.

[11] As we will show in forthcoming work, other proposals on the table would require an 85 percent vote of the IMF membership, a hurdle that is very difficult to jump.

[12] The alternative of relying on “internal” IMF resources for the subsidy and reserve accounts would require special majority votes, complicating approval and almost certainly entailing serious delay in setting up the GRT.

Topics

CITATION

Hicklin, John. 2021. Taking the Lead: Rechanneling SDRs to Create and Leverage a New Global Resilience Trust at the IMF. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.