Recommended

Event

Mobilizing and Allocating External Financing for Africa

VIRTUAL

March 17, 2021 9:30—11:00 AM ETGovernments have implemented an array of interventions needed to contain the economic impacts of COVID-19. Some of these interventions are not adequately captured in traditional fiscal metrics, such as debt and deficit. One approach to ensuring comprehensive coverage of these interventions and to prevent the build-up of fiscal risks is the adoption of a public sector balance sheet framework. The framework entails substituting debt as the main indicator of the financial position of the government with “net worth.” While there are significant challenges in compiling reliable balance sheets in African countries, the benefits of basic balance sheet analysis are within reach. Moving the agenda forward to ensure broad-based adoption of this comprehensive framework would entail enhanced collaboration between the IMF and the World Bank in nailing down the key challenges that could impede the adoption of such a framework; provision by these two institutions of tailored-made technical assistance and capacity development; facilitation of cross-country sharing of experiences; on-going collaboration with African regional organizations such as the AfDB; and securing the buy-in of country authorities, particularly through the involvement of civil society organizations and other fiscal watchdogs.

Background and context

Fiscal authorities have undertaken innovative and considerable policy interventions to mitigate the economic and financial fallout associated with the COVID-19 pandemic. Such interventions have prevented more severe economic contractions and larger job losses. During 2020-21, Nigeria implemented 2.4 percent of GDP in various forms of fiscal interventions to contain the economic impact of the virus, and South Africa spent about 6 percent of GDP. Equity, loans, and guarantees were also used in the case of South Africa, amounting to about 4 percent of GDP. The below-the-line interventions are not adequately reflected in the usual traditional macroeconomic indicators such as the debt-to-GDP ratio. To be more precise, a loan guarantee put in place to support the economy, for example, would only impact debt-to-GDP if a loss is realized. It has been well recognized that this form of policy intervention could potentially have a significant effect on public finances if it materializes. During the 1990-2014 period, 230 contingent liability realizations occurred with estimated average fiscal cost of about 6 percent of the affected country’s GDP (Bover et al., 2016). In this context, it is of utmost importance that country authorities adopt a balance-sheet approach to fiscal analysis and reporting to ensure comprehensive coverage and avoid build-up of fiscal risks.

The use of a balance-sheet approach in fiscal policy analysis could potentially provide a unifying framework for a better understanding of public sector operations. In the case of Nigeria, there seems to be two broad views on public-sector borrowing. One group is of the view that borrowing is needed to finance public investment, given the magnitude of infrastructure gap in the country. The other group maintains that public sector borrowing is not sustainable, given the ratio of interest payments to revenue. At the federal government level in 2021, interest payments as a share of revenue were about 86 percent. In addition, pubic gross debt has increased to 36 percent of GDP in 2021 from 23.4 percent in 2016.[1] These opposing views could be brought together via the application of a balance-sheet approach. Such an approach would allow for a specific answer to a simple policy question: is additional borrowing enhancing public sector net worth or compromising it? The unifying framework basically focuses on the long-term balance sheet-implications of how borrowed money is used.

Public sector balance sheet: Framework

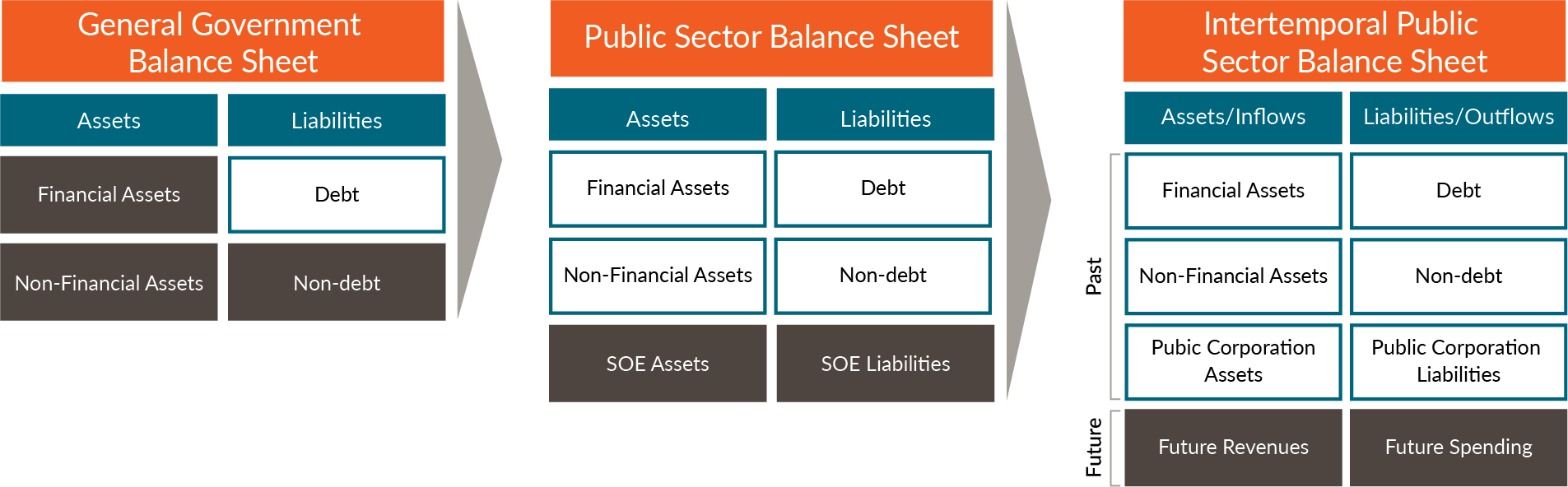

The adoption of a balance sheet approach entails substituting debt as the main indicator of the financial position of government with “net worth,” with attendant positive implications. Net worth captures the difference between the value of all assets and all liabilities. The balance sheet strength is not an end in itself, but a useful tool to facilitate the achievement of the objectives of public policy. In this regard, the net worth does not account for a country’s ability to tax in the future and / undertake needed expenditure adjustment. This is the reason why an intertemporal balance sheet analysis which integrates current wealth with future revenue and expenditure is equally important.

The public sector balance sheet (PSBS) framework extends institutional coverage beyond general government to include state-owned enterprises and financial public corporations including the Central Bank, which are often excluded in fiscal analysis (Figure 1). While these enterprises could possibly represent a significant asset for the government, they can also generate significant claims on budgets—often governments accumulate fiscal risks in these entities that will need to be addressed in the future. The PSBS framework provides an assessment of the scale and nature of public assets and non-debt liabilities and permits a more systematic assessment of the impact of policies on public finances by taking into account their short- and long-term effects on both asset and liability sides of the balance sheet.

Figure 1. Main elements of the balance sheet framework

Benefits of a balance sheet approach

Public sector balance sheets (PSBSs) provide the most comprehensive picture of public wealth. As a result, they account for the entirety of what the public sector owns and owes, providing a broader fiscal picture beyond debt and deficits (IMF, 2018). Due to its comprehensive nature, PSBSs equally bring about improved transparency and greater scrutiny of the government’s financial position. They also facilitate better balance sheet management, thereby reducing risks and the costs of borrowing. Countries with stronger balance sheets have been found to pay lower interest on their debt (Hadzi-Vaskov and Ricci 2016; Henao-Arbelaez and Sobrinho 2017).

Once governments have a better understanding of the size and nature of public assets, they can start the process of managing them more effectively, potentially generating substantial additional revenue. This is particularly relevant in Nigeria, where total revenues as a ratio of GDP reached about 7.4 percent of GDP in 2021. In addition, in the aftermath of the pandemic, governments are expected to focus on stabilizing their spending with a view to repairing their balance sheets. It is clear that some mixture of reduced public spending and tax increases will be required in the near to medium term in many countries. One additional element that could be taken into consideration is the adoption of a balance-sheet approach. This could allow for maximizing the return on public assets, resulting in increased domestic resource mobilization.

Balance sheet approach and African countries

There are challenges to be addressed in adopting a balance sheet approach to fiscal policy making in African countries. Some work will be required to make available the data needed to estimate the value of public assets and liabilities. The fiscal authorities will have to ensure that the data are of relatively good quality. In addition, a decision will have to be made on the appropriate methodology for estimating these public assets and liabilities. It is important to recognize that the balance-sheet approach is premised on accrual accounting. However, countries operating on a cash basis can apply the framework of balance-sheet management to their decision-making process.

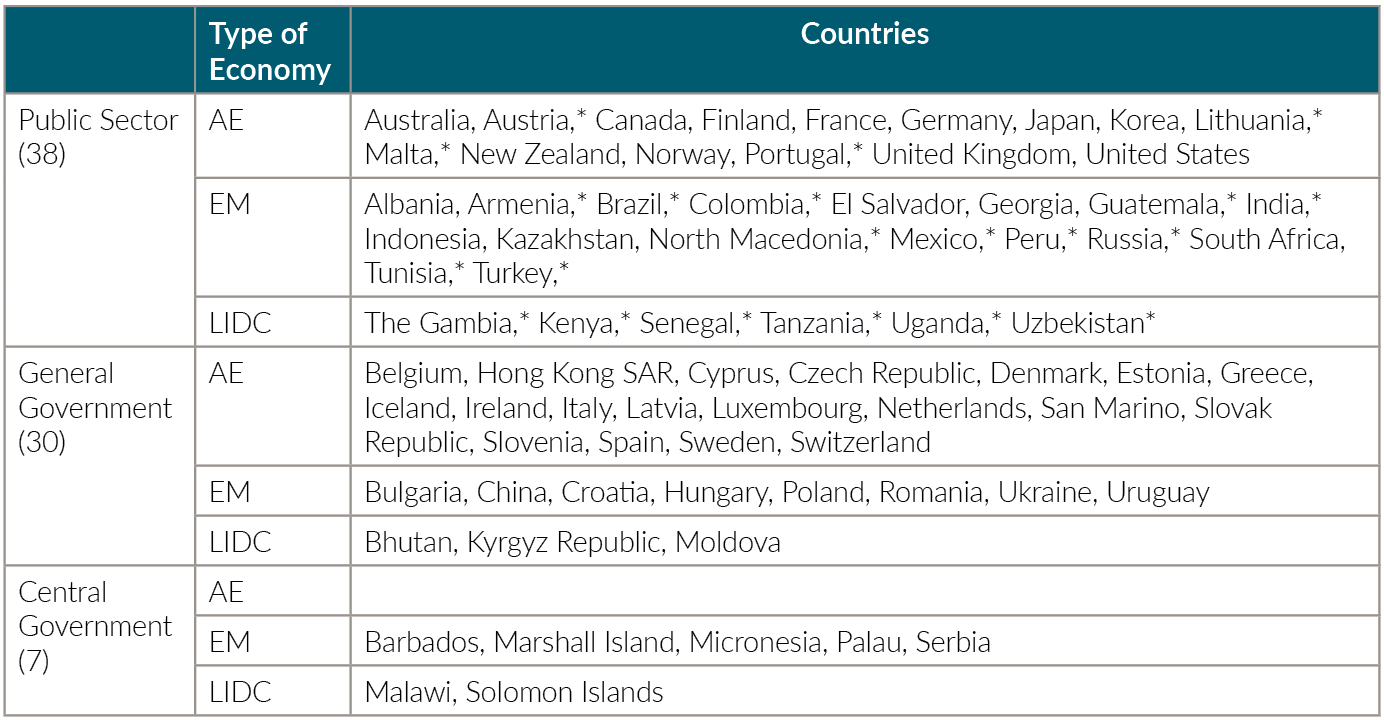

Public sector balance sheets have been compiled for six African countries (Table 1). These countries are: The Gambia, Kenya, Malawi, Tanzania, Tunisia, and South Africa. This demonstrates that with the buy-in of the fiscal, monetary and statistical authorities, there could be a broad-based adoption of a balance sheet approach to fiscal analysis in African countries.

Table 1. Public sector balance sheet database coverage

*Based on a single year of data, in most cases compiled as part of the Fiscal Transparency Evaluation.

Source: International Monetary Fund, 2019: Public Sector Balance Sheet Database.

Conclusions and next steps

While it is crystal clear that there are significant challenges in compiling reliable balance sheets, the benefits of basic balance sheet analysis are within reach of many African countries. To strengthen public accounts and to ensure effective design and implementation of fiscal policy, emphasis needs to be placed on promoting a medium-to-long-term balance-sheet oriented approach to policy making. High-quality PSBs are modeled on the financial reporting requirements that are common for private-sector organizations.

Moving the agenda forward to ensure increased adoption of the public sector balance approach in conducting fiscal policy would require the following:

- Enhanced collaboration between the IMF and World Bank. Increased collaboration between the International Monetary Fund and World Bank Group (Calderón and 2020; and World Bank, 2020) in view of the works they have done separately could help provide the framework for assessing the current state of play in African countries and identify specific measures required to effectively adopt a balance sheet approach to fiscal analysis.

- Criticality of technical assistance and capacity development. There exists scope for the IMF and World Bank to further provide tailored-made technical assistance in the area of public sector balance sheet framework. This could be complemented with helping to build human capacity through focused training for staff in finance ministries and statical authorities.

- Cross-country sharing of experiences. Public sector balance sheets have already been compiled for a few African countries. The IMF and World Bank could potentially facilitate collaboration between African countries that already have public sector balance sheets and those that are yet to do so.

- Collaboration with African regional organizations. The AfDB (2021) recommends that policy discussion should not be circumscribed to debt management and debt sustainability analysis in gross terms and that a more holistic approach to address fiscal and debt risks and vulnerabilities should gradually move from public debt management to public balance sheet management. This demonstrates scope for the International Financial Institutions to collaborate with the AfDB in bringing about a broad-based application of public sector balance sheet framework.

- The buy-in of country authorities in adopting a more comprehensive fiscal framework underpinned by the balance sheet approach is equally crucial. The process of adoption could be accelerated via the involvement of civil society organizations and other fiscal watchdogs, demanding for more comprehensive public sector data and analysis.

References

Adedeji, O.S. 2021, “The Sustainability of Government Balance Sheet in the Context of Covid Uncertainties” Being a Presentation Delivered at the 62nd Annual Conference of the Nigerian Economic Society, October.

African Development Bank. 2021, “African Economic Outlook”, 2021.

Calderón, C., and A. G. Zeufack. 2020, “Borrow with Sorrow? The Changing Risk Profile of Sub-Saharan Africa’s Debt”, Policy Research Working Paper 9137, World Bank Group, Washington, DC.

Bover, E., M. Ruiz-Arranz, F. Toscani, and H. E Ture. 2016, “The Fiscal Costs of Contingent Liabilities: A New Data Set”, IMF Working Papers 16/14, International Monetary Fund, Washington, DC.

Hadzi-Vaskov, M., and Luca A. Ricci. 2016. “Does Gross or Net Debt Matter More for Emerging Market Spreads?” IMF Working Paper 16/246, International Monetary Fund, Washington, DC

Henao-Arbelaez, C., and N. Sobrinho. 2017. “Government Financial Assets and Debt Sustainability.” IMF Working Paper 17/173, International Monetary Fund, Washington, DC.

International Monetary Fund, 2018, Fiscal Monitor: Managing Public Wealth. Washington, DC, October.

World Bank, 2020, “Government Financial Reporting in Times of the COVID-19 Pandemic”, Government Policy Note. Washington, DC.

[1] Debt figures include overdrafts from the Central Bank of Nigeria.

Topics

CITATION

Adedeji, Olumuyiwa. 2022. Pandemic, Debt Accumulation, and a Balance Sheet Approach to Fiscal Analysis in African Countries . Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

{kind=link}

{kind=link}