Recommended

Blog Post

The Evolution Roadmap Versus the Forward Look

Blog Post

CGD Podcast: Accelerating MDB Reform

In the field of development finance, the challenge of marshalling private investment in support of development goals is among the most vexing, and one that World Bank President Ajay Banga—a former Mastercard executive—has touted as a top priority.

Early in his tenure, Banga convened a group of CEOs (the private sector investment lab) to solicit their views on how the World Bank can better address investment barriers in client countries. Their first proposal, announced in late February, is to merge the Bank’s guarantee offerings. The reform will simplify things for clients and support Banga’s goal of tripling issuances to $20 billion annually by 2030. It is also a welcome step because guarantee uptake at the World Bank remains low, even though the instruments offer significant benefits to clients, including financial mobilization.

The risk is that speed and volume targets alone could fuel competition with private actors in established markets, undercutting the World Bank’s development mandate. Just as essential is a focus on impact. This can be achieved, at least in part, by including targets on where the Bank Group should scale (e.g., low-income countries). Country-based targets are consistent with current practice—the Bank’s private sector arms, the International Finance Corporation (IFC) and the Multilateral Investment Guarantee Agency (MIGA)—have each adopted business targets in the poorest economies and fragile and conflict states (FCS).

Scaling up in these economies is hard—deals are fewer, smaller, and riskier. But that is the nature of development finance, and these are development organizations.

To support both volume and impact goals, Banga should be open to greater risk appetite and commit to review the range of impediments to a more risk-tolerant culture, including decision-making structures, incentives, provisioning, and pricing. The imperative of maintaining the World Bank Group members’ AAA ratings means that proposals to relax constraints around risk taking are often met with stiff resistance. Unfortunately, this reflexive pearl clutching hampers thoughtful debates about where there is scope to increase appetite without imperiling the AAA ratings. As we discuss in this paper, there are good options for reasonably and responsibly enabling a more risk tolerant culture. Moreover, absent some increase in risk appetite, the private sector agenda is again likely to fall well short of expectations.

The private sector agenda so far: big ambition, disappointing outcomes

The criticality of private sector mobilization to development finance is not new—indeed this was the rationale for establishing the IFC in 1956 and MIGA in 1987. But the focus on private finance intensified after the adoption of the Sustainable Development Goals (SDGs) in 2015 due to their stratospheric price tag.

In 2015, the World Bank and other major multilateral development banks (MDBs) issued the “Billions to Trillions” report on their shared plans for supporting the SDGs. A key assertion was that by “catalyzing, mobilizing and crowding in,” they could leverage their capital several times over, trumpeting that “for every 1 dollar invested directly by MDBs in private sector operations, some 2-5 dollars are mobilized in additional private investment.”

To lure private capital where it otherwise might not go, development finance institutions offer incentives like guarantees, insurance, and equity. But their use remains limited, and own-account finance has not translated into trillions of development dollars. Instead, on average each dollar of public investment catalyzes roughly another sixty to seventy cents.

Risk avoidance has been a significant obstacle to achieving better outcomes—a problem embedded in MDB financial and operational models (and described in this experts’ group report). To be fair, it is not clear whether any development financial institution, including the IFC, can leverage $2-$5 dollars per $1 of investment, as there was never a good evidence base underpinning the “billions to trillions” proposition. But there is no doubt that the current record can be significantly improved upon.

Doubling down

Despite a disappointing track record, the private-sector agenda remains top of mind, at least in part because development funding gaps are huge and it’s proving tough to move the needle on other major sources of finance: official development assistance(ODA) and domestic resource mobilization (DRM).

Total ODA in 2022 reached $211 billion—a record high, but after accounting for inflation an funds to pay for refugee-hosting costs, this figure quickly loses its luster. It is also a small fraction of estimated needs, which are in the trillions of dollars and rising. In addition, the OECD’s 1970 target of allocating 0.7 of a member country’s gross national income for ODA has lost all credibility: in 2022, it was met by only four countries.

Domestic resource mobilization also remains stubbornly low in the region where needs are greatest—sub-Saharan Africa (SSA). In its latest regional outlook the IMF estimated that revenues in SSA hover around 17 percent of GDP on average and increased by only one percent between 2019 and 2023. This compares to 27 percent and higher in emerging markets and advanced economies.

In contrast, private flows are growing significantly as a share of developing country finances. A World Bank study on the composition of public sector financing in developing countries found that private flows between 2010 and 2019 grew five times faster than official finance, rising from 36 to 50 percent as a share of total financial flows. The fact that the private sector is the largest and most dynamic source of funding is not the only source of its appeal. By focusing on this agenda, budget-constrained donors can deflect attention away from ODA funding pressures.

What we know so far about the Bank’s renewed private-sector agenda

During a Council on Foreign Relations event in 2023, Banga telegraphed two key goals: one is to get the IFC to work “much faster, much quicker” and with a greater sense of urgency. Another is to help manage extreme risks that “almost no one knows how to factor into any kind of spreadsheet,” such as outsized foreign exchange or political risk.

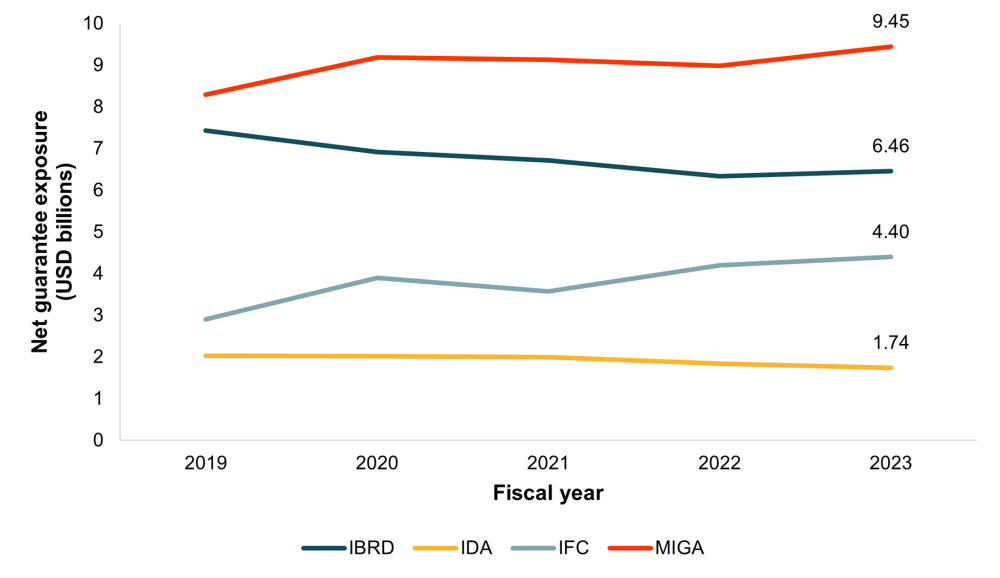

Following consultations with the advisory group Banga assembled (his private sector investment lab), the World Bank announced its first big reform: a consolidation of twenty guarantee products from both the sovereign and private arms covering financial, policy and political risks into one unit, and a streamlined process for accessing them. This is good news for clients because institutional constraints, including the decentralized structure, have discouraged their use- currently guarantees represent only 3.2 percent of total exposure.

Figure 1. WBG guarantees

Source: WBG financial statements.

Moving the agenda forward

What comes next will be key to finding out just how ambitious and robust the new private sector reform agenda is. A top priority should be to confront the World Bank Group’s low-risk-appetite culture and related issues, including provisioning, pricing and incentives. But Banga was notably antagonistic on the subject during a fireside chat at CGD, saying:

“Look, I think this thing of everybody telling the World Bank to take more risk is one of the bigger jokes that I've heard in my life. And the reason that that's a joke is if we actually booked that risk as a loss, you're going to have to replenish my capital so that I can remain Triple-A rated. Try getting a dollar of capital right now. So to pass the buck around is not a good way to solve a problem. This is like passing the parcel, and one day the music will stop and people are going to be left holding the parcel. So I don't have time for that kind of conversation. And I tell all the larger shareholders, please don't talk to me about risk unless you're willing to back up the capital that otherwise may need to be taken.”

Banga’s mental sprint from taking more risk to booking that risk as a loss is a puzzling leap, considering the World Bank Group’s outstanding credit history, including in high-risk environments. There is a large gulf between taking additional risk and imperiling the AAA rating. And shareholders are pressing the Bank to do more. During the 2023 Annual Meetings of the World Bank and IMF, for example, US Treasury Secretary Janet Yellen urged MDBs to “develop scalable platforms to increase private investment, including securitization platforms, and... scale and better utilize guarantees, insurance, local currency lending, and other de-risking tools to crowd-in investors.”

Andrew Mitchell, the UK Foreign Secretary, had this to say: “The World Bank must also mobilise significantly more private capital, including through bringing all of the Group together to drive this agenda, building stronger pipelines of projects, innovating to develop new instruments and vehicles to securitise MDB assets, and deploying the full range of tools including local currency finance and guarantees.”

The case for more risk

To my mind, a frank conversation between Banga and the Bank’s Executive Board about what is acceptable in terms of risks and losses in the context of AAA ratings is overdue. Credit rating agencies factor shareholder support into their calculations, so seeking a public show of shareholder endorsement as part of any agenda around risk appetite would also be a shrewd move.

Determining a threshold for risk appetite is not easy, especially in the absence of data on defaults and recoveries—which the IFC does not provide-- a transparency gap I have ranted about separately. Nevertheless, a case for more risk appetite is not hard to make, as discussed below:

The International Finance Corporation

In 2023, IFC investments in the poorest countries (i.e., those with access to IDA, the concessional lending arm of the World Bank) fell to a record low of 8.8 percent of total IFC business after peaking at nearly 23 percent in 2018.

Table 1. IFC investments in IDA countries

|

Fiscal Year |

IDA countries |

Total IFC |

IDA share |

|---|---|---|---|

|

2015 |

1,891.28 |

9,460.91 |

19.99% |

|

2016 |

2,031.75 |

12,576.87 |

16.15% |

|

2017 |

1,358.60 |

11,115.54 |

12.22% |

|

2018 |

3,558.17 |

15,514.09 |

22.94% |

|

2019 |

1,247.32 |

8,305.75 |

15.02% |

|

2020 |

1,575.76 |

10,023.70 |

15.72% |

|

2021 |

1,355.79 |

10,829.41 |

12.52% |

|

2022 |

1,151.36 |

10,300.95 |

11.18% |

|

2023 |

1,457.09 |

16,584.98 |

8.79% |

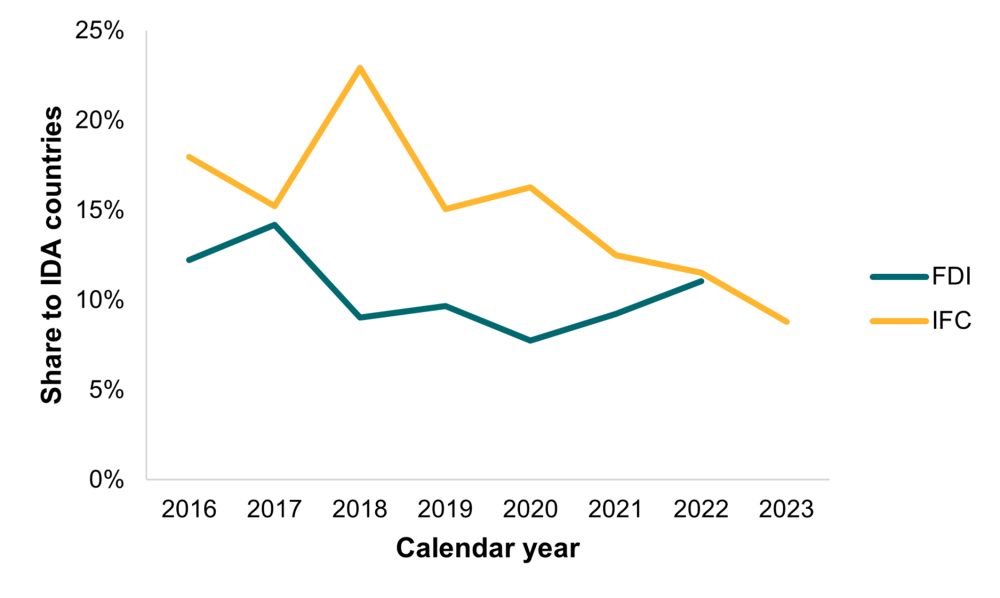

This is an especially sobering figure in the context of IFC’s goal to deliver 40 percent of its long-term finance in IDA-eligible and fragile and conflict-affected states by 2030. But as my CGD colleagues discuss here, IFC’s track record of meeting commitments in low-income markets has never been stellar. Also notable about this trend is that IFC investments in IDA markets are declining while private flows are on the rise.

Figure 2. IFC versus private flows into IDA countries

Source: IFC Financial Summary; World Bank World Development Indicators.

Note: FDI data represents the share of global FDI net inflows made up by IDA countries; IFC data represents the share of total IFC investments in IDA countries; adjustments are made to reflect changes in IDA eligibility. 2023 private flow estimates are not yet available.

Absent more insight into what caused the steep decline in these markets, it is difficult to propose a strategy for regaining ground. But assessing risk tolerance at the IFC should certainly be in the mix.

The Multilateral Guarantee Insurance Agency

To reach Banga’s goal of increasing guarantee issuances from $6.8 billion to $20 billion per year by 2030, MIGA will have to play an outsized role. MIGA provides guarantees against political risk and non-payment risks of sovereigns and sovereign entities (like state-owned enterprises), but it cannot offer the latter product in any country with a credit rating below BB-. This restriction covers most of MIGA’s client countries, posing a significant constraint to its potential growth. As I have argued here, it makes eminent sense to replace what is now a binding constraint on MIGA’s ability to operate with a policy that enables staff to exercise their judgement on a case-by-case basis, and yet this reform has gotten no traction.

The Private Sector Window

World Bank shareholders will soon consider how to reform the Private Sector Window (PSW), a $6.7 billion facility financed by IDA that was set up six years ago to enable higher-risk private investments in IDA countries. The PSW is not constrained by the IFC’s AAA rating and is provisioned for 100 percent losses. And yet evidence shows that risk appetite remains unacceptably low—to date, the PSW has paid out only $1 million in guarantees, or less than one percent of total exposure. There is ample room to reduce provisioning and assume more risk, steps that IDA deputies should take during the upcoming replenishment.

Conclusion

Risk is the main constraint to private investment in emerging markets and developing countries. The World Bank has a robust toolkit for mitigating and sharing risk to enable better capital intermediation in support of development objectives. But its ambitions are not being met.

The good news for Banga is that he has strong support for leading a reinvigorated private sector agenda. But early indications are that he is focusing too narrowly on process and scale. Absent a commensurate emphasis on development impact, staff will be motivated to find deals where private markets are already well established, undermining the IFC’s major strategic goal of developing “new and stronger markets for private sector solutions” in IDA-eligible and fragile and conflict-affected countries, and imperiling MIGA’s ability to scale quickly without compromising its development objectives. This will not please stakeholders.

To avoid this outcome, the World Bank needs to relax the institutional brakes on risk taking—something that can be done without accelerating to unsafe speeds. The urge to dig in and protect the status quo runs deep within the World Bank but ironically this course poses its own risk, which is that Banga’s private sector agenda will stutter and stall.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: Skórzewiak / Adobe Stock