The market value of the IMF’s gold—about US$170 billion at end 2020—far exceeds its historic cost on the Fund’s balance sheet of under $5 billion. Not surprisingly, this has led some to see the IMF’s gold as a “free” resource that should be tapped to meet pressing global needs. And these calls have become louder as the demands of meeting new challenges—from climate change to the pandemic—have confronted flat or shrinking aid budgets.

It is certainly possible for the IMF to sell gold, and significant profits from gold sales have in recent years bolstered the IMF’s concessional support for low-income countries (LICs). But a range of issues—legal, political, and practical—constrain how the IMF’s gold has been and could be used. While the details may seem arcane, they are important. Indeed, a recognition of the constraints helps focus attention on desirable options that could be attainable. Drawing on our new note, “Financing a Possible Expansion of the IMF’s Support for LICs,” we highlight the main constraints, starting with those hardwired into the IMF’s charter, called the Articles of Agreement.

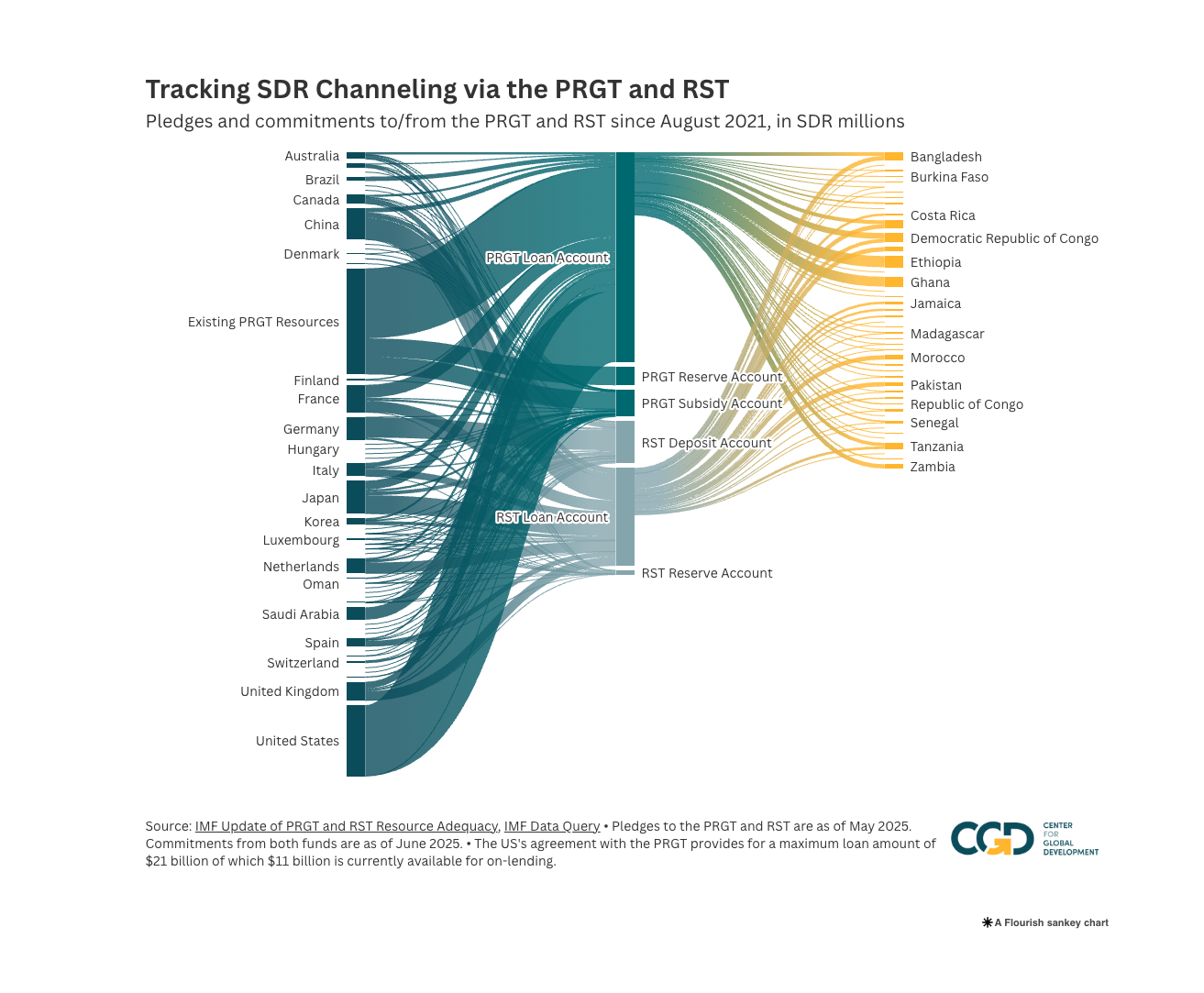

-

The IMF can conduct outright gold sales only with the support of a super majority of 85 percent of the IMF's Executive Board. This high threshold means that the support of the US, which also requires congressional backing, is essential, and other coalitions of countries could easily block sales. Moreover, the IMF does not have the authority to engage in other transactions such as loans, leases, swaps, or the use of gold as collateral that could leverage the high market value of its gold holdings.

-

The Articles of Agreement strictly limit the use of profits from gold sales. The vast bulk, if not all, of the IMF’s gold was acquired before the Second Amendment to the Articles of Agreement in 1978. The Articles provide for profits from this “pre-second amendment” gold to be transferred to the Special Disbursement Account (SDA) and used to provide concessional balance of payments assistance to IMF members. However, a further stipulation is that gold sales profits in the SDA be used only for operations and transactions that are consistent with “the purposes of the Fund” as defined in Article 1. Accordingly, this architecture would not appear to support the use of gold sales profits to, for example, provide an earmarked fund to support directly climate or health spending. Relaxing this constraint would require an amendment to the Articles. Ratification of even seemingly noncontentious amendments typically requires months, if not years, given the need to obtain acceptance is from three-fifths of the membership accounting for 85 percent of the voting power (a double super majority).

The high threshold of support required to approve sales also brings to prominence other policy considerations.

-

The IMF’s gold holdings are seen as providing fundamental strength to its balance sheet. Since the last financial crisis IMF’s total lending capacity of US$1 trillion has been justifiably stressed as a bulwark for global financial stability. This capacity for the most part represents quota resources and borrowing agreements that the IMF can draw upon from member central banks. In intermediating these resources, the IMF—essentially the international lender of last resort to countries in distress—carries the risks of this lending so that central banks can in turn carry the resources lent to the IMF on their books at their full face value. In this context the IMF’s (undervalued) gold holdings are seen as providing an additional and vitally important backstop to support the IMF’s unique financing mechanism. This risk-bearing role does not preclude gold sales, but it has been interpreted by many IMF shareholders as sharply limiting the scale of such sales.

-

Avoiding disruption to the gold market is an important facet of the IMF's policy on gold sales. The gold market is an unusual commodity market in that (aboveground) gold stocks are very large in relation to annual mining output. As a result, the gold price can be very sensitive to changes or expected changes in gold holdings, including holdings by the IMF. Assuaging concerns over potential market disruption is likely to remain important in gaining political support for any gold sales. The world’s five largest gold producing countries account for about 30 percent of the voting power of the Fund’s Executive Board and thus could block any gold sales (which require an 85 percent vote). Therefore, selling the Fund’s gold in a way that does not disrupt commercial markets is critical. And again, the larger the sales the larger the likely impact on the gold price.

Despite these difficulties, gold sales have been used to support LICs and could be used again.

-

In 1999-2000 the IMF sold about one-eighth of its gold holdings to help finance the debt relief provided to LICs under the Heavily Indebted Poor Countries initiative (HIPC). The scale of this operation was consistent with the IMF's policy of holding relatively large amount of gold for prudential reasons. Between December 1999 and April 2000, separate but closely linked transactions involving a total of 12.9 million ounces of gold were carried out between the IMF and two member countries that had financial obligations falling due to the IMF. In the first step, the IMF sold gold to the member at the prevailing market price and the profits, totaling just over SDR 2.2 billion, were placed in the SDA. In the second step, the IMF immediately accepted back at the same market price the same amount of gold in settlement of the members’ financial obligations. Since the net effect of these transactions in 1999-2000 was to leave the IMF’s gold holdings unchanged, they did not affect the global gold market.

-

The IMF’s concessional lending under the Poverty Reduction and Growth Trust (PRGT) has been ramped up dramatically to support LICs in the pandemic. But this level of support is not sustainable over the longer term without new unencumbered resources to meet the subsidy cost of PRGT lending (as we discuss in “Financing a Possible Expansion of the IMF’s Support for LICs.”) How much is needed will only become clear over the next year or two but could likely be covered by sales no larger than in 1999-2000.

-

An operation similar to that conducted in 1999 to 2000 could in principle be used to provide new subsidy resources for the PRGT. As well as Executive Board support of 85 percent, this would require agreement from a member or members to purchase gold from the IMF at market prices and then immediately use this to settle forthcoming loan repayments to the IMF. This would have the advantage of not affecting the gold market as IMF holdings would again be unchanged.

-

Building support for gold sales will not be easy. In the best of circumstances, it will likely take years not months to gain this support and then plan and conduct the required sales. As we argue in our paper, there are ways to support the PRGT as a bridge to financing from gold sales. But the foundation for this—progress towards gold sales—should be laid now.