Recommended

At the start of the COVID pandemic, we examined how major deteriorations in low-income country (LIC) debt levels could influence the grant funding requirements for IDA, the World Bank’s low-income-country lending arm. IDA provides a mix of concessional credits (which need to be repaid) and grants (which do not) to eligible countries, depending on the country’s economic situation. That means that as country debt situations worsen, IDA’s mix automatically shifts to a higher proportion of grants, which are more costly to provide.

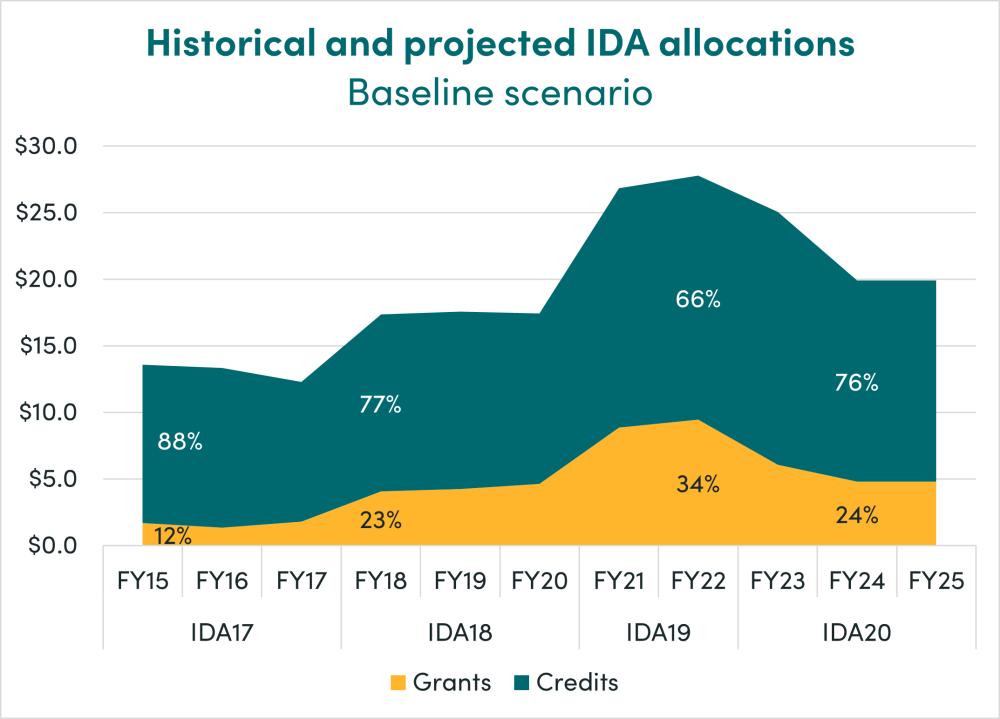

In 2020, IDA was providing a bit under a quarter of its country policy-based allocation (PBA) as grants. But as debt dynamics continued to worsen during the global pandemic, some of our “bad case” scenarios bore out. By 2022, the share of IDA’s core finance provided as grants increased to over a third. In IDA 20, the replenishment cycle currently underway, IDA donors have adopted stricter rules for grants, which we estimate could bring the grant-share back down to a quarter of the PBA. But if debt dynamics continue to worsen, the claim on grants will again grow, which would place further strain on IDA’s finances. It would also raise difficult questions around who will bear the burden: donors or the poorest?

IDA: A model responsible lender

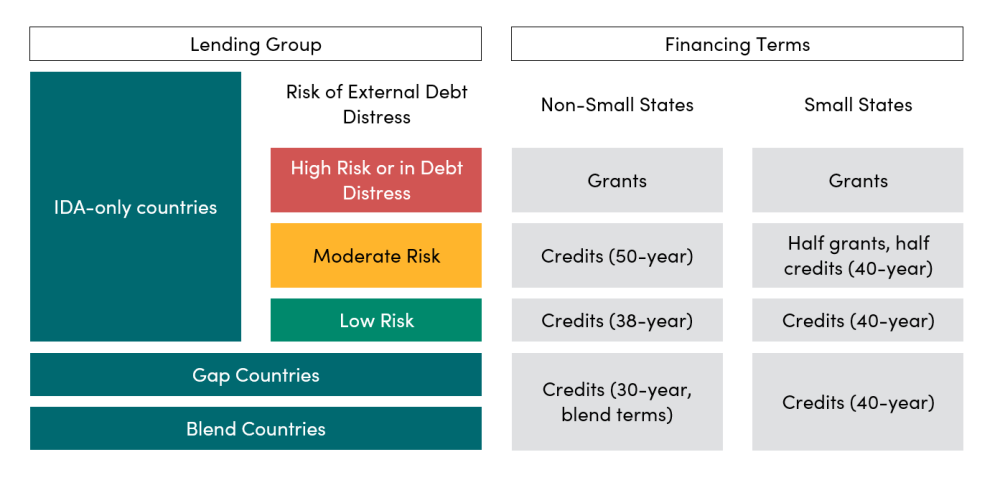

A core feature of IDA’s lending is that it modulates loan terms to country debt levels. Historically, IDA has provided credits to countries at low risk of debt distress and grants to countries at high risk of debt distress. For countries at moderate risk, IDA recently switched from providing a mix of credits and grants to providing 50-year credits with no service charge or interest rate. “Gap” and “Blend” countries, (i.e., countries currently above the IDA operational threshold of GNI per capita of $1,315 but not creditworthy enough to access the IBRD, or countries that are “creditworthy but do not meet the income threshold”) are only eligible for loans, regardless of their risk of debt distress. There are various exceptions to these rules for small economies (see table below).

Table 1. Summary of IDA20 financing terms

Source: IDA-20 Deputies Report

This framework ensures that IDA is not contributing to deteriorating debt dynamics—but it is expensive and comes at a cost. Grants are net losses for IDA since, unlike credits, they do not flow back and cannot be rechanneled as new commitments.

Three scenarios: baseline, borderline, b-line

Source: IDA country allocations, authors’ projections

Notes: Non-core IDA country allocations (including regional allocations, the Crisis Response Window, the Scale Up Facility, and the Private Sector Window) are not included in this chart. The projections for IDA 20 assume a $2.7 billion decline in IDA PBA between FY22 and FY23 and $5.2 billion decline in FY24 and FY25.

Over the past three IDA replenishment cycles, debt dynamics in low-income countries have worsened. At the beginning of IDA 17, the replenishment cycle that ran from mid-2014 to mid-2017, 17 countries were at high risk of debt distress and 12 percent ($1.7 billion a year) of core IDA funding was in grants. By the end of IDA 19, 38 countries were at high risk of debt distress and over a third of IDA core funding was in grants, about $9.5 billion a year in annual commitments.

Due to the decision to change countries at moderate risk of debt distress from a mix of credits and grants to pure concessional terms for IDA 20, the grant component has likely reverted to IDA-18 levels (i.e., around a quarter of the PBA going out as grants).

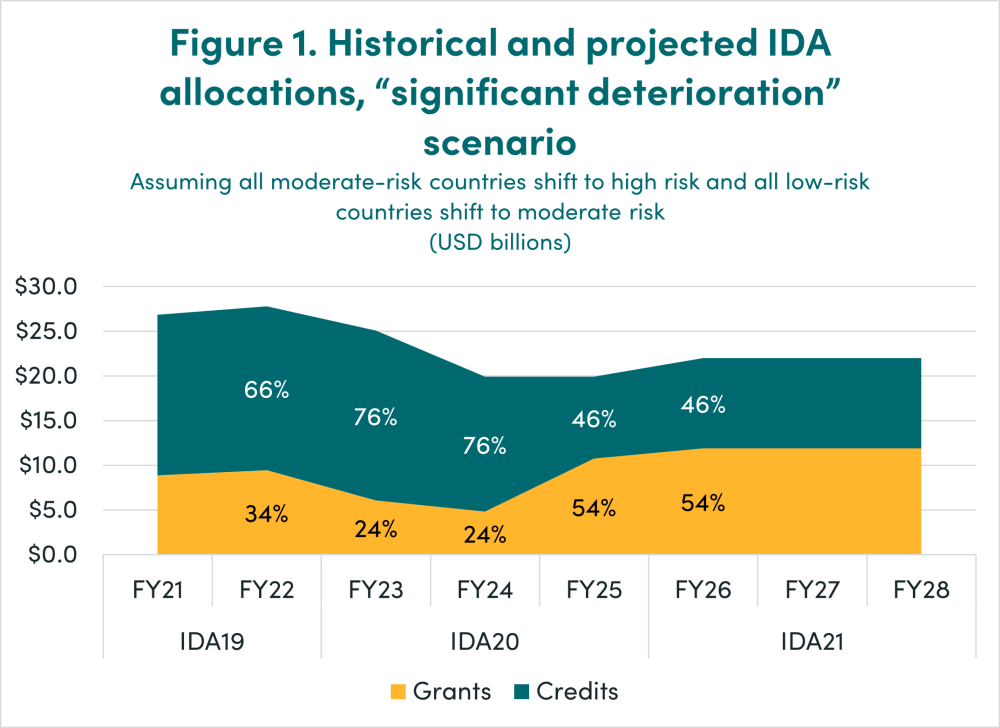

But what happens to the grant levels for the remainder of IDA-20 and the next replenishment cycle if country debt ratings continue to deteriorate? We ran two scenarios: one based on a significant deterioration and the other on a catastrophic deterioration. In both cases we kept the distributions of the PBA constant using FY22 as the baseline year.

First, we assume that every country at moderate risk becomes high risk starting in FY25. Here the grant share of IDA’s PBA for the remainder of IDA 20 more than doubles from 25 percent to 54 percent. The claim on grants would surpass the IDA 19 high watermark and could reach almost $11 billion a year. Looking forward to IDA 21, this could amount to almost $36 billion in grants for the cycle. (For IDA 21, we assume PBA levels are an average of the projected annual PBA levels of IDA 20).

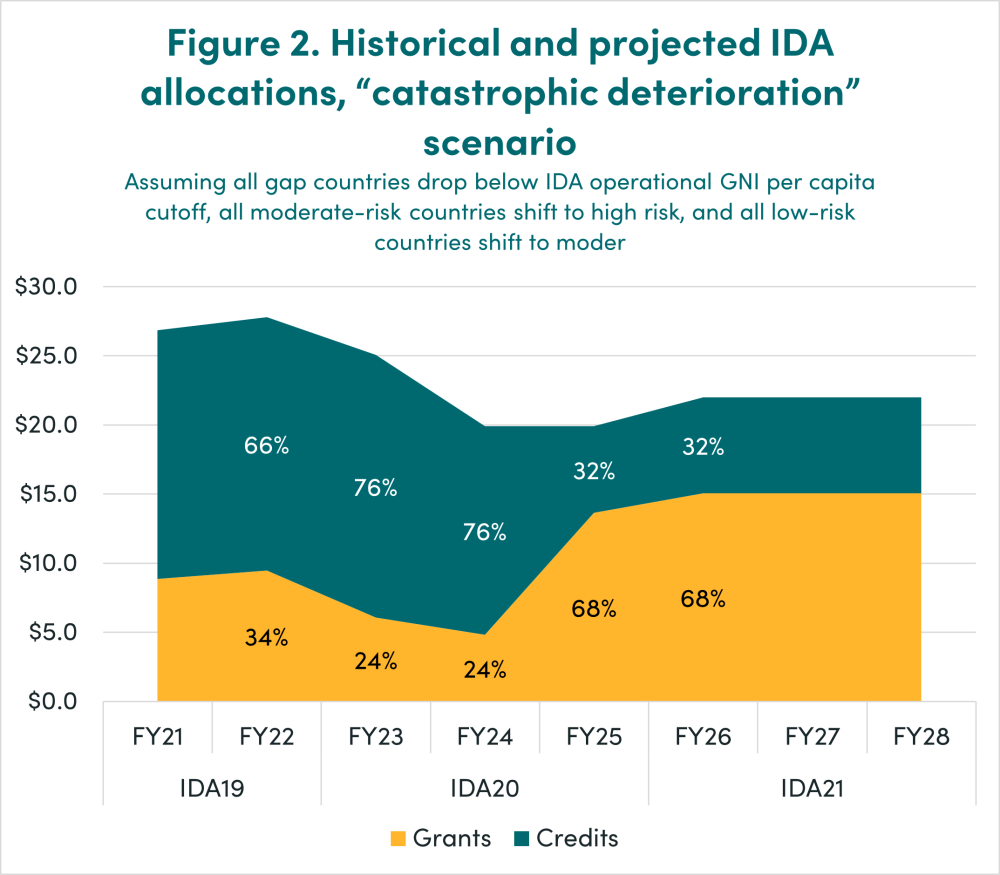

Our second scenario is more catastrophic. Starting in FY25, on top of the deteriorations described in the first scenario, all Gap countries would also drop below the per capita IDA income threshold. This would make them eligible for grants according to their debt risk weightings, which would also deteriorate by one risk category (e.g., if a Gap country was at moderate risk of debt distress, it is now high risk). Under this scenario, nearly 70 percent of IDA’s financing would go out as grants in FY25—almost $14 billion. This would translate to an eyepopping $45 billion over the course of the IDA 21 cycle.

These simplified scenarios underscore how responsive IDA’s model remains to deteriorating economic and debt circumstances. In fact, our projections likely underestimate the overall size of the annual grant program since they do not include grants allocated through set-asides like the crisis response or regional windows. We also include an overall drop in lending in FY24 and FY25 in our projections since IDA is expected to have to reduce lending to accommodate for the frontloading in FY23.

Can IDA afford a surge in grants in IDA 20 and beyond?

IDA has historically provided most of its funding as credits. As a result, IDA currently has over $185 billion in outstanding loans which reflow to the organization. IDA reflows are now the single largest source of financing for IDA, more than donor grant contributions. A key tradeoff at play is between volume and terms: any increase in grants reduces IDA’s future commitment authority. But there’s a time lag: most IDA loans have a significant grace period (6-10 years) and extended maturity periods, so an increase in the grant program would not affect reflows until 2-3 replenishments in the future. (And ditto for a hardening of terms.)

For IDA 20, IDA received $23.5 billion from donors in grants. If IDA’s annual grant program is beneath donor grant contributions, IDA can afford its grant program without dipping into its equity base. That is the case in the baseline scenario, where the grant program is around $15 billion. But in both of our stress scenarios, the grant program for IDA-21 would vastly exceed the IDA-20 levels of donor grants. Donors would need to increase their contributions by $12 billion (the first scenario, “significant deterioration”) to $22 billion (the second scenario, “catastrophic deterioration”) or dip into IDA equity to cover.

|

Estimated IDA 20 Source of Finance ($B) |

|

|---|---|

|

Partner grant contributions |

23.5 |

|

Borrowing |

33.5 |

|

Internal resources (includes reflows, carry forward and internal transfer) |

36 |

|

Total |

93 |

Source: IDA 20 Deputies Report and CGD staff estimates

In recent cycles it made sense for IDA to partially alleviate the volumes/term tradeoff by increasing its market borrowing program, blending market financing with grants to reach concessional terms. But IDA’s funding costs have gone up significantly in a higher global interest environment, and most countries need grants or highly subsidized lending, which also require a heavy grant component.

Measures to further contain the growth in grants, like restricting their eligibility to an even narrower subset of IDA countries, are likely to be hotly debated in the IDA 21 replenishment negotiations. But if donors are committed to preserving IDA’s character as a model of responsible lending, they will need to signal willingness to bankroll the grant program, whatever it takes.

Thanks to Karen Mathiasen for helpful comments on an earlier iteration of this blog.

Disclaimer

CGD blog posts reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions.

Image credit for social media/web: Who is Danny / Adobe Stock