Last Friday, the Government of Belize alongside the U.S. Development Finance Corporation (DFC) and the Nature Conservancy (TNC) announced the financial close of the largest blue bond for Ocean Conservation to date. The program enables Belize to convert its existing Eurobond (i.e., foreign currency bonds issued on the international market) into blue debt that it will use to implement its national marine conservation agenda. This program is part of a global TNC Blue Bond for Conservation program. If DFC is to be judged on its strategic use of risk sharing tools, its systemic impact on a highly vulnerable country, and its readiness to build a replicable model with a globally respected partner like TNC, this transaction should get a top score.

Debt-for-nature swaps are appealing financing mechanisms that help governments, including highly indebted governments, address several different challenges at once: lowering unsustainable debt stocks and debt service burdens, encouraging private participation in debt restructuring, and incentivizing use of fiscal savings for green (or blue) investments. This isn’t only an appealing arrangement for governments and donors but can also be enticing for creditors who can recoup a portion of their investment.

Debt-for-nature instruments are not new to the scene, but they have gained fresh attention in the context of looming debt crises in many low-income countries and the urgency of the climate crisis. Combining debt relief with climate progress offers an elegant solution to two systemic crises. But to have a systemic effect, they must be replicable and scalable. Are they?

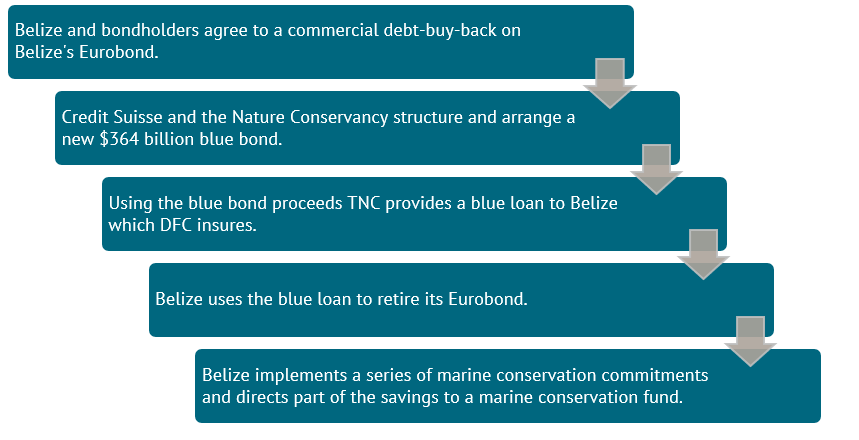

Let’s look at how the debt for marine conservation swap in Belize works. Belize had $553 billion in Eurobonds that were trading at a steep discount. (If a bond is trading below its value, it means the bondholders believe that the creditor will not be able to honor its repayment). The public debt of Belize stood at 125 percent of GDP. Belize and its bondholders agreed that Belize would repurchase the outstanding debt for about 55 cents on the dollar. (Nearly 85 percent of bondholders agreed to the arrangement.) This agreement allowed the government of Belize to reduce its external debt stock by a sizable nine percentage points of GDP. To repay bondholders, TNC issued a blue bond and passed on the proceeds to Belize in the form of a blue loan. DFC then provided political risk insurance to enhance repayment prospects for the new debt, which helped enable an investment grade rating for the TNC blue bond. The government of Belize then used the blue loans to retire the Eurobond at a discount.

Using part of the fiscal savings from the bond restructuring, the government of Belize agreed to implement tangible coastal and marine conservation measures, including increasing biodiversity protection zones from 15.9 percent of ocean area today to 30 percent by 2026. (See a full list of commitments here.) The government will also establish a Conservation Fund that will be capitalized by the government of Belize to the tune of $180 million in payments over 20 years. The Conservation Fund will be an independent entity that is neither controlled by the government of Belize nor by TNC. Both government and non-governmental organizations will be eligible to apply for funding for coastal conservation projects. Hopefully the Fund will be structured in such a way that applicants will have to compete for access to funding, increasing changes for maximizing conservation benefits relative to funding costs.

This blue bond program is the largest of its kind to date. Previously, the TNC had worked with the government of the Seychelles on a similar (albeit much smaller) $18 million program that was guaranteed by the World Bank. DFC had also previously worked with TNC on blue bond marine conservation programs for Kenya and Saint Lucia. DFC’s predecessor OPIC provided political risk insurance for a program in Barbados. More broadly, debt-for-nature swaps have been in the mix for some time but their uptake has been fairly limited in scope.

With half of low-income countries in or at risk of debt distress and many of the same countries highly vulnerable to climate-related risks, debt-for-nature swaps and climate bonds once again feature prominently in the debt and climate debate. A key question is whether these type of operations—adapted to different country circumstances as blue or green finance mechanism—could offer a workable and widely applicable blueprint to help countries reprofile or even retire their commercial debt burdens.

But momentum for this type of approach seems to be fraying. The IMF postponed unveiling a debt-for-climate swap program with the World Bank at COP26 due to limited progress on a specific proposal. While there are successful examples of climate debt swaps, they have been small, can have high transaction costs, and have uncertain private creditor interest. The Belize transaction took time to construct, partly because it required building consensus across diverse natural capital stakeholders in Belize, balancing commercial with conservation interests.

But debt-for-climate advocates and naysayers alike should certainly take close look at the Belize blue bond. By virtue of its size, it has considerably improved Belize’s macroeconomic outlook and helped drive an ambitious government-led conservation agenda. This benefit should help dispel the notion that such swaps can only be limited to small transactions or cannot be done in highly indebted countries. Moreover, getting 85 percent of creditors to agree to such a deal is no easy feat: after all creditors did agree to forfeit 45 percent of their initial investment. Skeptics might do well to note the contrast between the Belize success and the very slow pace and scope of debt restructuring under the G20 Common Framework which has yet to complete a successful restructuring. As countries like Zambia struggle with their own Eurobond repayments, might they and their creditors see some appeal in a Zambian Green Bond deal?

Note: On 11/10/21, we edited this blog to correct a numerical error regarding the purchasing of Belize's debt.

El pasado viernes, el gobierno de Belice y la Development Finance Corporation de Estados Unidos (Financiera para el Desarrollo, en español y DFC por sus siglas en inglés) y The Nature Conservancy (La Conservación de la Naturaleza, NTC) anunciaron un acuerdo en relación con el mayor bono azul hasta la fecha. Este programa permitirá a Belice convertir su eurobono (un bono en moneda extranjera emitido en el mercado internacional) en deuda azul que usará para implementar su agenda nacional de conservación marina. Este programa es parte del programa global de TNC Blue Bond for Conservation (Bono Azul para la Conservación, en español). Esta transacción y la DFC merecen una matrícula de honor por el uso estratégico de herramientas para compartir el riesgo, su impacto estructural en un país altamente vulnerable y por ofrecer modelos replicables en colaboración con socios respetados a nivel internacional.

Los debt-for-nature (deuda por naturaleza) swaps son unos atractivos mecanismos financieros que ayudan a los gobiernos, incluso a aquellos con altos niveles de deuda, a lidiar con varios problemas al mismo tiempo. Permiten reducir stocks de deuda insostenibles y la carga del servicio de la deuda, animan a los acreedores privados a participar en las reestructuraciones de deuda e incentivan el uso de ahorros fiscales para inversiones verdes (o azules). Estos acuerdos no son solo atractivos para los gobiernos y los donantes, sino que también pueden serlo para los acreedores que pueden usarlos para recuperar una parte de sus inversiones.

Los instrumentos de debt-for-nature no son nuevos, pero están volviendo a ganar relevancia en un momento en el que las crisis de deuda acechan a numerosos países de ingreso bajo y en el que aumenta la gravedad y la atención sobre la crisis climática. Combinar las medidas de condonación de deudas con el avance la agenda climática es una solución elegante a dos crisis sistémicas. Pero, para que estos instrumentos tengan un efecto sistémico y estructural, deben ser replicables y extensibles. ¿Lo son?

Veamos cómo funciona el swap de deuda por conservación marina de Belice. Belice tenía 553 mil millones de dólares en eurobonos que estaban en el mercado con un descuento muy grande. (Que un bono esté siendo vendido por debajo de su valor significa que los poseedores del bono no creen que el prestatario vaya a poder hacer frente a sus pagos). La deuda pública de Belice alcanzaba el 125 por ciento del PIB. Belice y sus acreedores acordaron que el país recompraría la deuda pendiente por un 55 por ciento de su valor. (Casi el 85 por ciento de los acreedores aceptaron este plan). Este acuerdo permitió al gobierno de Belice reducir su stock de deuda externa en un sustancial 9 por ciento del PIB. TNC emitió un bono azul y pasó las ganancias a Belice a través de un bono azul. A continuación, la DFC aportó un seguro de riesgo político para mejorar las perspectivas de repago de la nueva deuda, lo que a su vez permitió que el bono azul de TNC lograra un “investment grade” (grado de inversión, en español). Por último, el gobierno de Belice usó el bono azul para retirar los eurobonos con un precio descontado.

Usando una parte del ahorro fiscal que supuso la reestructuración de los bonos, el gobierno de Belice accedió a implementar medidas de conservación marina y de la costa significativas y tangibles. Estas medidas incluyen incrementar las zonas de protección de la biodiversidad del 15.9 por ciento del área oceánica actual a un 30 por ciento en 2026 (se puede ver una lista completa de todos los compromisos aquí). El gobierno también establecerá un Fondo de Conservación que tendrá un capital de entorno a los 180 millones de dólares a lo largo de 20 años. El Fondo de Conservación será una entidad independiente que no estará controlada ni por el gobierno de Belice ni por TNC. Tanto el gobierno como organizaciones no gubernamentales podrán solicitar financiación para proyectos de conservación de la costa. Esperamos que el Fondo se estructure de tal manera que los solicitantes tengan que competir para acceder a financiación, lo cual maximizaría los beneficios de conservación de una manera eficiente, teniendo en cuenta los costos.

Este tipo de programa de bonos azules es el más grande hasta la fecha. Anteriormente, TNC había trabajado con el gobierno de Seychelles en un programa similar, aunque mucho más pequeño, de 18 millones de dólares que fue garantizado por el Banco Mundial. La DFC también había trabajado en el pasado con TNC en programas de bonos azules de conservación marina en Kenia y Santa Lucía y OPIC (el predecesor de DFC) aportó un seguro de riesgo político en Barbados. Los swaps de debt-for-nature llevan dando vueltas algún tiempo, pero su adopción ha sido limitada.

Estos swaps han ganado relevancia en el debate sobre la deuda y el cambio climático en un momento en el que la mitad de los países de ingreso bajo se encuentran a punto enfrentar problemas de sobreendeudamiento (o ya los están enfrentando). Una pregunta clave es si este tipo de operaciones—adaptadas a las circunstancias de distintos países como mecanismos de financiación verdes o azules—pueden ofrecer una solución práctica y ampliamente aplicable para ayudar a los países a reconfigurar y o incluso disminuir sus cargas de deuda comercial.

Sin embargo, el “momentum” de este tipo de acuerdos parece estar decayendo. Em el COP26, y debido al escaso avance a la hora de especificar la propuesta, el FMI ha pospuesto el lanzamiento de un programa de swaps de debt-for-climate (deuda por clima) con el Banco Mundial. Aunque hay ejemplos exitosos, estos han sido pequeños, con grandes costos de transacción e incertidumbre acerca del interés de los acreedores privados. La transacción de Belice tomó tiempo, en parte porque hubo que buscar un consenso entre las diversas partes interesadas, logrando un balance entre los intereses comerciales y los de conservación.

Pero tanto los que apoyan los swaps de debt-for-climate como sus detractores deberían examinar el bono azul de Belice. Sólo gracias a su tamaño ya ha mejorado considerablemente las perspectivas macroeconómicas de Belice y ha ayudado a impulsar una ambiciosa agenda de conservación liderada por el gobierno. Estos beneficios deberían eliminar la noción de que este tipo de swaps se tienen que limitar a transacciones pequeñas y de que no se pueden lograr en países altamente endeudados. Más aún, es destacable que el 85 por ciento de los acreedores estuvieran de acuerdo con este trato tras ceder el 45 por ciento de su inversión inicial. Los escépticos deberían tomar nota del contraste entre el éxito de Belice y el lento proceso de reestructuración de deuda del G20 que todavía no ha completado ninguna reestructuración. Países como Zambia siguen teniendo dificultades a la hora de repagar sus eurobonos. ¿Quizás tanto el gobierno de Zambia como sus acreedores puedan ver ahora el valor de un bono verde?

Nota: el 10 de noviembre de 2021 editamos este blog para corregir un error numérico sobre la deuda de Belice.

Disclaimer

CGD blog posts reflect the views of the authors, drawing on prior research and experience in their areas of expertise.

CGD is a nonpartisan, independent organization and does not take institutional positions.

Image credit for social media/web: nr_photos/Adobe Stock