Recommended

POLICY PAPERS

The Addis Ababa Agenda for financing development pays special attention to domestic revenue mobilization to help finance the Sustainable Development Goals (SDGs) in developing countries. In the case of sub-Saharan African countries, much of the discussion has centered on improving their overall revenue performance, and while they have, there is still a long way to go. Based on our findings in a new paper examining the extent to which institutional and political factors explain tax rates in sub-Saharan Africa, we argue here that countries in the region searching for higher revenues to finance investments in the SDGs do not have to raise tax rates. Lower tax rates can deliver the desired amount of revenue, provided certain institutional and political considerations are aligned appropriately.

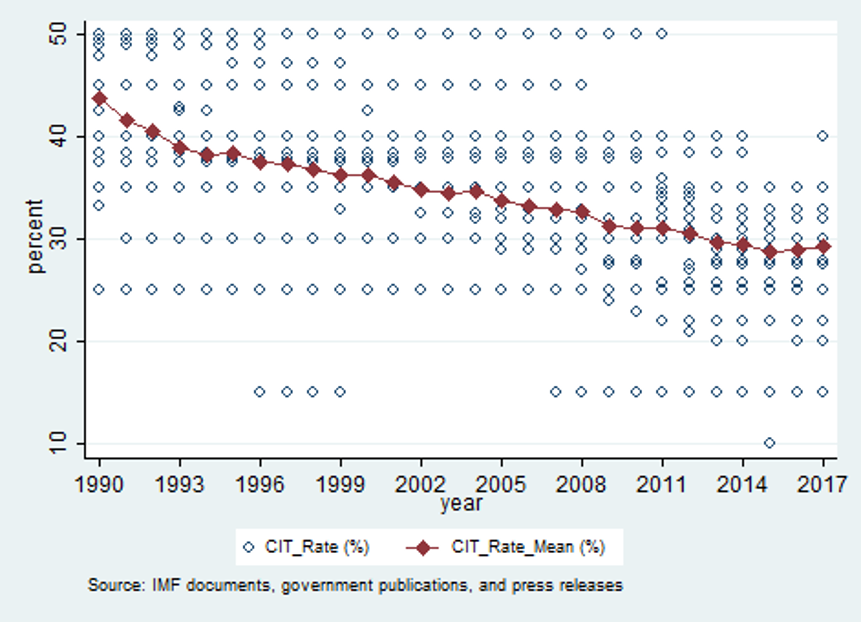

The revenue performance of sub-Saharan Africa as a region has improved over the past 30 years. Figure 1 shows unweighted average tax revenue from personal income tax, corporate income tax, and value-added tax (VAT) as a percent of GDP in sub-Saharan Africa from 1990 to 2017. During this period, VAT revenue increased by about 3 percent of GDP, despite the fact that VAT rates have remained broadly unchanged since the early 1990s (figure 2). The increase in VAT revenue is attributable to expanding consumption in the formal/taxed sector and improved tax compliance. Personal income tax revenue also increased by about the same amount during 1990–2017, reflecting implementation of more progressive tax systems even though top marginal tax rates declined (figure 3). Corporate income tax revenue went up by a percentage point of GDP, despite falling corporate income tax rates (figure 4).

Figure 1. Personal income tax, corporate income tax, and VAT revenue as a percent of GDP in sub-Saharan Africa, 1990-2017

Figure 2. VAT rates in sub-Saharan Africa countries 1990-2017

Figure 3. Top marginal personal income tax rates in sub-Saharan African countries, 1990-2017

Figure 4. Corporate income tax rates in sub-Saharan African countries, 1990-2017

Institutional and political considerations and tax rates in sub-Saharan Africa

Two considerations can affect tax rates in a country. On the one hand, well-functioning institutions and regulations can translate tax rates into an efficient revenue system. The stronger these institutions, the lower tax rates need to be to generate one additional dollar of revenue. On the other hand, political considerations linked to political tenure, fragmentation, and electoral and ideological considerations of the party in government can affect tax policy rates. In our paper, we investigate the extent to which these considerations explain statutory tax rates in sub-Saharan Africa.

Key findings

Our empirical analysis is confined to corporate and personal income tax rates because VAT rates have remained stationary over the time period studied, making it impossible to use quantitative techniques for analysis. Our investigation shows that in countries with weak institutions and poor regulatory quality, corporate and personal tax rates tend to be higher. Similarly, weak accountability driven by longer tenures of a veto player—someone who can stop a change from the status quo—is positively linked to higher tax rates. It is possible that such long-lasting political actors grant tax exemptions to benefit political allies that support their long tenure. We find that lower accountability associated with longer tenures of key veto players tends to have a greater impact on tax rates, even when a country has a sound regulatory quality. Weak revenue administration capacity and pervasive tax evasion, which are typical of more authoritarian regimes, are probably behind this result.

Fragmented or polarized governments tend to have higher corporate tax rates and personal tax rates; that is, they have more progressive tax systems. And contrary to results from advanced economies, the ideological orientation of the government does not have an effect on statutory tax rates. The relationship between electoral cycles and tax rates is weak, although we find some evidence that governments are more likely to increase corporate tax rates the year after a legislative election.

What does this mean for policy?

Three important policy implications can be drawn from these results:

First, sub-Saharan African countries do not need to raise their tax rates to generate higher revenues; they should focus instead on improving their regulatory quality.

Second, a moderate degree of political stability helps in maintaining a modest level of tax rates; both a long tenure by the same party in government and too much political volatility linked to party fragmentation can lead to higher tax rates.

Finally, elections and ideology are not significant factors affecting underlying tax rates in the region. Regardless of political discourse on this matter, evidence shows that these two variables have not been a major determinant of sub-Saharan African tax policies in the last three decades.

For more details on our analysis and findings, read the full paper here.

Disclaimer

CGD blog posts reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions.